China is exiting a prolonged period of cement sector growth. The consequences could be far reaching, both at home and abroad...

With an estimated population of 1.4bn in 2018, China is the most highly-populated country in the world. It is also the fourth largest by area. With a centrally-planned economy and low cost of production, the country became a major manufacturing base during the 20th Century, although an emerging middle class, associated rising wage demand and increasing environmental concerns are gradually eating into China’s historical advantage in this area. The country’s former ‘one child policy’ (1979 - 2015) has resulted in a rapidly-ageing population. As a result, the Chinese population will shrink by 60 million by 2050.

Cement industry introduction

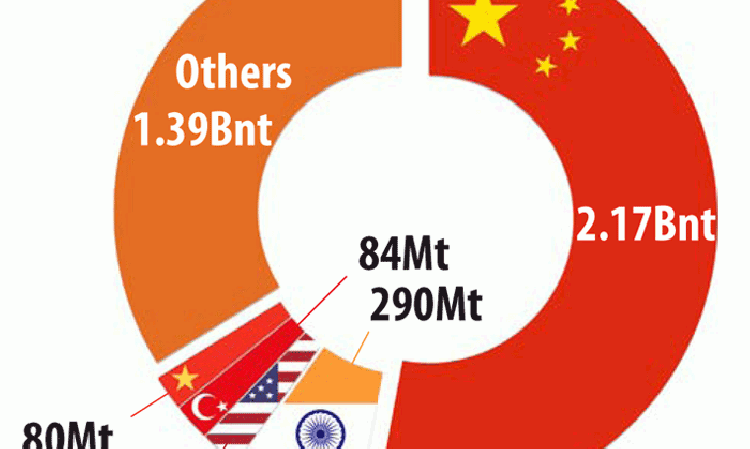

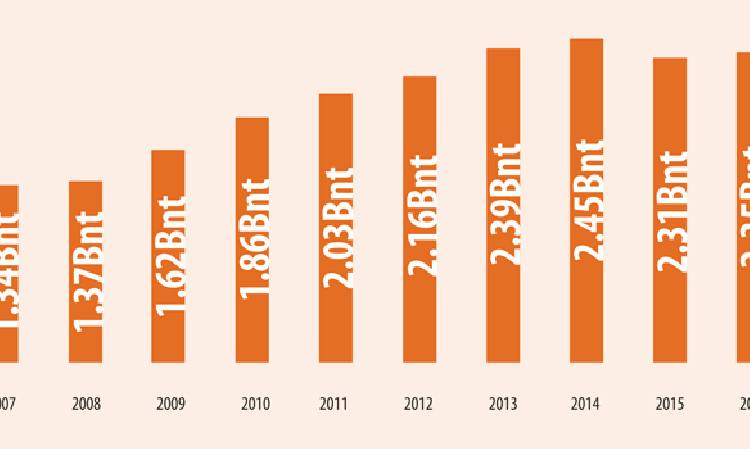

Chinese cement production is the world’s largest by a significant margin, as shown in Figure 1, a situation that has been the case for the whole of the 21st Century. From 1995 production rose from 500Mt/yr to over 1Bnt/yr in the decade to 2005. Between 2005 and 2015 cement production in China further increased by a factor of 2.5, hitting 2.45Bnt in 2014. It produced more cement than the rest of the world combined for the first time in 2007.

According to official statistics, China sold 2.17Bnt of cement in 2018. Despite this incredible number, nearly 53% of global cement production for the year, cement sales actually fell by 6.1% in China in 2018 compared to 2017. Indeed, since 2014 the sector’s output has contracted by around 300Mt, more cement than second-placed India makes in a year.

Stopping the overcapacity supertanker

China’s cement sector grew very rapidly in the early 2000s to match the country’s rapid urbanisation drive. However, a severe overshoot has resulted in excess building stock, sometimes entire empty cities, and vast cement overcapacity. Warnings were sounded as early as 2003, when the country still made less than 1Bnt/yr of cement. In 2012 the National Bureau of Statistics of China (NBSC) officially warned that too much cement was being made and, in 2013, China’s State Council issued the ‘Guideline to tackle serious production overcapacity,’ including in the cement sector. At the same time, the Chinese Cement Association (CCA) drafted plans to promote mergers and acquisitions in the sector.

In 2017 the CCA elaborated on its plans, stating that 393Mt/yr of clinker capacity and 540 small to medium-sized cement grinding plants would be closed by 2020. The aim is to reach clinker and cement utilsation reates of 80% and 70% respectively. For reference, CNBM had a capacity utilisation rate of ~63% in 2017.

Efforts to reduce production have variously included forced closure of older capacity, bans on new plants and expansions and forced campaign production around major cities. Each of these has tied in with China’s increased environmental focus. A ban on 32.5 grade cement brought in in December 2015 is estimated to have sidelined more than 340Mt/yr of capacity alone.

A complete ban on new capacity was announced by the Ministry of Industry and Information Technology (MIIT) in February 2018. The MIIT stated at the time that any new cement-making projects that are ‘absolutely necessary’ must follow replacement capacity rules, “To ensure that the total production capacity will only decrease and not rise.”

The focus on consolidating major players has accelerated in recent years, with the conclusion of the CNBM-Sinoma merger in 2018. This deal, which began in August 2016, has created by far the largest cement producer in the world (521Mt/yr).

Producers’ domestic fortunes

The overcapacity situation in China’s cement sector has led its cement producers on a financial rollercoaster over the past five years. After a poor 2015, in which China National Building Materials’ (CNBM) profit slumped by 83% to US$157m and Anhui Conch’s profit fell by a third to US$1.16bn, China’s cement makers set about repairing their balance sheets in 2016. Anhui Conch’s revenue rose by 9.7% to US$8.12bn in 2016, while its profit increased by 14% to US$1.24bn. CNBM saw its revenue rise, albeit by just 1%. 2017 confirmed that producers had been able to steady themselves after the peak of 2014. CNBM reported sales of US$20.3bn for the year, roughly twice as much as Anhui Conch (US$12bn), which in turn reported sales twice as large as China Resources Cement (CRC) (US$3.8bn).

However, what was more interesting in 2017 was the trend towards higher prices in the wake of capacity reduction measures, an effect mentioned by CNBM in its annual report. The year was also notable for a distinct increase in the number of projects that Chinese cement producers are involved in overseas, more on which below.

Cement price rises continued to boost Chinese cement producers in 2018, despite the slowdown in sales gaining pace. Indeed, many producers issued positive ‘profit alerts’ towards the end of 2018 that were subsequently followed up by significantly improved financial reports.

Data from the National Development and Reform Commission in February 2019 showed that the profits of Chinese cement producers had more than doubled to US$64bn in 2018, predominantly on the back of price rises (a note on which is below). The effects of capacity reduction are clear, even if it is hard for those outside of China to verify the scale of the reduction.

Looking at individual firms, there was a 19% year-on-year rise in sales revenue at China National Building Material Company (CNBM) to US$32.6bn in 2018 from US$27.4bn in 2017. Its profit grew by 44% to US$2.09bn from US$1.46bn. Anhui Conch’s performance was even better. Its revenue grew by 70.5% to US$19.1bn from US$11.2bn.

Prices increase as supplies cut

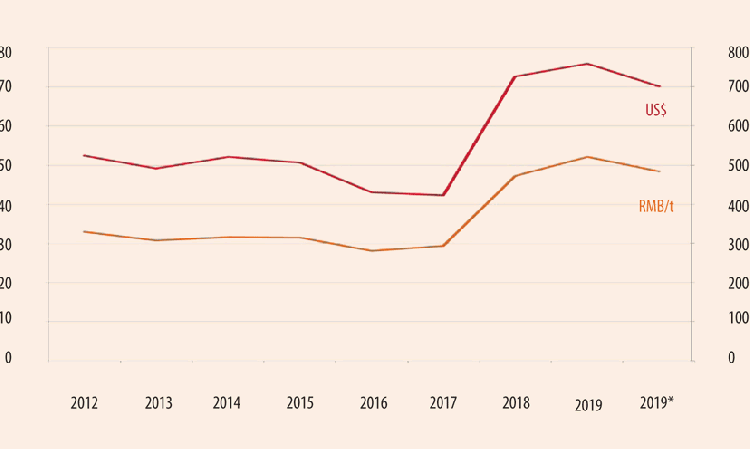

Cement prices have historically been lower in China than in many other places around the world due to oversupply. Figure 3 shows the price of cement in China over the past six years in US$/t and Chinese RMB/t. Prices gradually declined over the four years from 2012 to 2016, from US$52/t (RMB330/t) to US$43/t (RMB281/t). However, since a marginal increase in RMB terms at the start of 2017 (a fall in US$ terms), they have jumped by 77% to reach US$76/t (RMB552/t) in January 2019. The price has since fallen to US$70/t (RMB485/t) on 5 June 2019.

Figure 3 clearly shows the effects of decreased supply within the Chinese cement market. It has helped raise the profitability of China’s major state-owned producers, in line with government targets.

Expansion abroad

Having removed some of the ‘heat’ in its domestic cement sector over the past five years, the Chinese cement sector, as well as its many engineering firms, have been ramping up their activities outside of China, particularly since 2017. Late that year, Song Zhiping, the former chairman of CNBM, said that his company was planning to build 100 new plants in 50 countries by 2021.

Chinese companies are involved in a variety of projects, many of which are joint ventures. In 2018, Global Cement was made aware of 41 projects across north Africa (6), sub-Saharan Africa (8) the Middle East (2), South America (3) and central (7), north (3), south (6) and south east (6) Asia. These projects comprise 52.4Mt/yr of cement capacity in the form of new clinker lines, grinding plants and expansion projects that have been ordered, are under construction, were commissioned or entered into production in 2018.

In the five months to 31 May 2019, a further eight projects have been announced in six different countries. They encompass a further 17.1Mt/yr of new non-Chinese capacity in which Chinese firms are either the supplier, investor or both.

Chinese cement producers have even entered into formal partnerships with western suppliers. In May 2019 CNBM signed a strategic agreement towards climate change and cooperation in third countries with France’s Fives FCB. This agreement developed the collaboration plans drawn up in January 2019. The companies forecast a volume of business of at least Euro600m over three years, and forms part of CNBM’s stated strategy of developing in partnership with western companies. The agreement focuses on upgrading CNBM’s cement plants in China, building new plants outside of China and creating a Joint Engineering Centre to implement these projects and share information. Both parties were keen to point out that the agreement showed the ‘mutual trust’ between the two companies with respect to intellectual property.

Trump turns up tariff tiff tension

China and the United States have been involved in an escalating trade tariff war over the past 12 months. On 6 July 2018 China imposed a 25% tariff on 545 US products worth US$34bn in response to the US decision to collect a 25% tariff on US$34bn-worth of 818 separate Chinese products. In July and August 2018 the US proposed further lists of Chinese imports that might become subject to tariffs. In response China drew up a list of 5207 products from the US.

On 23 August 2018 a second round of tariffs were imposed by both sides to include a further US$16bn of products. As part of the US package, mineral products from China of interest to the cement industry subject to tariffs included limestone flux, quicklime, slaked lime, gypsum, anhydrite, clinkers of Portland, aluminous, slag, supersulphate and similar hydraulic cements, white Portland cement, Portland cement, aluminous cement, slag cement, refractory cements, additives for cement, cement based building materials and more.

In May 2019 it was announced that the Chinese Ministry of Finance had increased tariffs on selected US goods, including cement, to 25% with effect from 1 June 2019. The total number of products affected was not increased. The new Chinese tariffs range from 10% to 25% and include clinker, white cement, other Portland cements, other hydraulic cement, refractory cement, additives for cement, plaster and concrete, limestone, quicklime, slaked lime, gypsum, refractory products and cement packaging machinery.

The effects of these measures on the Chinese cement industry are difficult to assess but data from the United States Geological Survey (USGS) regarding Chinese imports into the US appears to point to a reduction in cement imports. Over the first six months of 2018, before the imposition of cement tariffs, the US imported 0.79Mt of Chinese cement, 23.4% more than in the first half of 2017. However, the second half was a different story. US imports of Chinese cement fell by 20.9% to 0.97Mt during the second half of 2018, from 1.2Mt in the second half of 2017. This significantly dampened the full year increase to 1.7%. However, over the first six months of tariffs, the period from September 2018 to February 2019, there was a 36% drop in imports compared to the September 2017 to February 2018 period. If sustained, this appears to indicate that US tariffs are impacting in a minor way on Chinese exports.

As at 6 June 2019 President Trump said that he was considering tariffs on a further US$300bn of Chinese goods, indicating that this dispute may be far from over.

Heading forwards... or back?

The deceleration of the Chinese cement sector since 2014 represents a major achievement but the measures taken to date will only go so far. Consider that 2Bnt of cement is enough for almost 1500kg for every one of China’s 1.44nb inhabitants. Even when southern Europe was in the building boom of the early 2000s, rates rarely hit half of that level. Many will claim that China’s size and centrally-led economy enables it to be a ‘special case,’ as over recent decades.

As economic growth slows and international tensions rise, the China Cement Association’s aim of 80% capacity utilisation seems to be a reasonable target. However, even if the cement sector was to continue to contract at 5%/yr, per-capita consumption won’t dip below 1000kg until the mid 2030s. China will have consumed another 20-25Bnt by then. Can any country really need that much cement? A western, market-economy mindset says, ‘Surely not!’ However, continued national development, mega-infrastructure projects, a shift to more exports and China’s unique economy could mean that the country continues to surprise the world for decades to come.

Lead article image by Picrazy2CC BY-SA 4.0