The global cement industry has seen a number of major combinations and divestments in recent years, including the formation of LafargeHolcim, the absorbtion of Italcementi into HeidelbergCement and, most recently, the ongoing merger between Chinese majors CNBM and Sinoma to form the largest cement producer in the world. Here we look at the current Top 10 global cement producers...

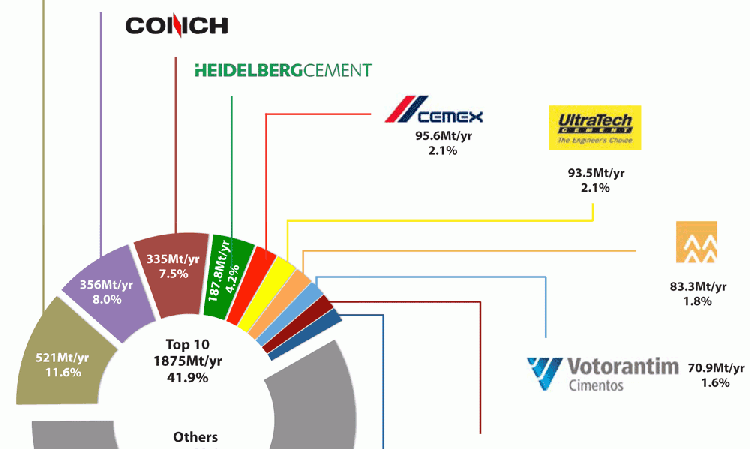

The Top 10 cement producers by installed capacity in 2018 are shown in Table 1 and Figure 1. Between them they share 1875.4Mt/yr of integrated and grinding capacity, around 41.8% of the 4470.3Mt/yr total cement capacity that is listed in the Global Cement Directory 2018. Information for Chinese and Taiwanese producers has been taken from respective company reports. The four Chinese and Taiwanese producers operate 1008.3Mt/yr of capacity between them, nearly 54% of the capacity held by the Top 10 cement producers and around 22.5% of all cement production capacity.

| Rank | Producer | Capacity (Mt/yr) | Share of global capacity (%) |

| 1 | CNBM / Sinoma | 521 | 11.6 |

| 2 | LafargeHolcim | 356 | 8 |

| 3 | Anhui Conch | 335 | 7.5 |

| 4 | HeidelbergCement | 187.8 | 4.2 |

| 5 | Cemex | 95.6 | 2.1 |

| 6 | UltraTech Cement | 93.5 | 2.1 |

| 7 | China Resources | 83.3 | 1.8 |

| 8 | Votorantim | 70.9 | 1.6 |

| 9 | Taiwan Cement | 69 | 1.5 |

| 10 | CRH | 63.3 | 1.4 |

| TOTAL | Top 10 | 1875.4 | 41.8 |

Above - Table 1: Top 10 cement producers in 2018, by installed cement capacity. Source: Global Cement Directory 2018, Global Cement research and company reports.

1. CNBM & Sinoma

CNBM, founded in 2004, operates 409Mt/yr of cement capacity solely in China via a number of subsidiaries. It is in the final stages of formally merging with fellow state-owned firm Sinoma, established in 1983, which has a capacity of 112Mt/yr. When the merger is completed, it will form a cement player with 521Mt/yr, by far the largest in the world, albeit one that only operates within China. The enlarged entity will maintain the CNBM name.

| HQ: China | China | 2017 Cement Production (CNBM): | 257.6Mt |

| Shared Capacity: | 521Mt/yr | 2017 Revenue (CNBM / Sinoma): | US$19.6bn / US$8.7bn |

China National Building Materials (CNBM) and Sinoma are in the final stages of becoming the largest producer of cement in the world by installed capacity (521Mt/yr). The two announced that they would merge in May 2018. However, there has been no formal announcement that it has been completed.

CNBM operates its cement interests via: 1. China United (100% stake): Encompassing capacity from more than 30 subsidiaries in Shandong, Jiangsu, Henan, Hebei, Anhui and Sichuan Provinces; South Cement (80% stake): Active in Zhejiang, Shanghai, Jiangsu, Anhui, Hunan, Jiangxi and Guangxi Provinces; North Cement (70% stake): A joint venture with Liaoyuan Jingang Cement and Hony Capital Management; Southwest Cement (88.7% stake): Capacity operated via Chongqing Kehua Group, Sichuan Lisen, Yunnan Simao Jianfeng Cement and Guizhou Taian Cement and others.

Sinoma also operates its cement production assets via four subsidiaries: Xinjiang Tianshan Cement (39.0Mt/yr), Sinoma Cement (24.0Mt/yr), Ningxia Building Materials (21.0Mt/yr), Quilianshan Cement (28.0Mt/yr).

Recent performance

CNBM had a strong year in 2017. It took revenues of US$19.6bn across all of its business lines, which include concrete, gypsum wallboard and wind turbine blade manufacturing, in addition to cement production. This revenue value was 25.7% more than the US$15.6bn that it took in 2016. CNBM’s net profit for the year was US$5.4bn, a 31.7% rise from the US$4.1bn that it made in 2016.

The group produced 257.6Mt of cement in 2017, broadly unchanged from 257.2Mt in 2016. There were more significant changes at two of CNBM’s subsidiaries. China United produced 1.9Mt more in 2017 (57.9Mt) than in 2016 (56.0Mt), a 3.4% rise year-on-year. Meanwhile North Cement’s production fell by 12.4%, from 19.1Mt in 2016 to 16.7Mt in 2017. South Cement’s production was unchanged year-on-year from 97.0Mt in 2016 to 97.1Mt in 2017. Southwest Cement’s production rose from 85.2Mt to 86.0Mt.

Sinoma took US$8.7bn in operating revenue in 2017, with cement production earning the group US$3.8bn (44%). Sinoma’s considerable cement plant engineering arm took US$3.2bn. The cement sector’s operating revenue in 2016 was US$3.0bn. The company reported that the increase was mainly due to higher selling prices.

Merger timeline

The merger between CNBM was announced by the Assets Supervision and Administration Commission in August 2016. The move is part of wider efforts by the Chinese government to consolidate the country as part of supply side reforms. The two firms entered into a merger agreement in September 2017, as a result of which Sinoma will be absorbed into CNBM. The exchange ratio for the deal is 1 Sinoma share to 0.85 of a CNBM share. This allocates 58.8% of the newly-enlarged CNBM to its existing shareholders.

The deal was approved by the Anti-monopoly Bureau of the Ministry of Commerce in mid-December 2017 and by the China Securities Regulatory Commission (CSRC) in March 2018. At this point the merger process appears to be nearing completion, although there has as yet been no formal announcement that the process is over.

Recent news

CNBM increased its share in Southwest Cement from 70% to 88.7% in June 2018.

Song Zhiping stepped down as director and the chairman of the board of directors of CNBM in mid-June 2018.

CNBM was among nine founding members that set up the Global Cement & Concrete Association at the end of January 2018.

2. LafargeHolcim

Three years after the formal merger of Lafarge and Holcim, the world’s largest multinational cement producer is still in a stake of consolidation and flux. There have been senior level changes, job losses and a financial loss in 2017.

| HQ | Switzerland | 2017 Cement Sales | 210Mt |

| Capacity | 356Mt/yr | 2017 Revenue | US$23.4bn |

LafargeHolcim traces its history back to the founding of Lafarge, in France in 1848 and Holcim in Switzerland in 1912. Each company grew through expansions and acquisitions around the world to become leading global cement producers by 2000.

LafargeHolcim was born through the merger of Lafarge and Holcim in July 2015. Its formation was prompted by both groups seeking to maintain their industry-leading positions and due to their complementary spread of assets around the world. The merger process was fraught at times, with Lafarge shareholders having to accept a minority stake in the new entity based on that company’s weaker-than-expected financial performance. Both firms were forced to sell assets in various countries to comply with local competition legislation. Asset sales have continued since the completion of the merger as the group seeks to streamline it operations in a competitive international market.

According to the Global Cement Directory 2018 LafargeHolcim’s headline capacity was 356Mt/yr. However, it sold just 210Mt of cement in 2017, a capacity utilisation rate of just 59%. In 2016 the company sold 233Mt of cement. It said that this was due to the sale of units in China, Chile and Vietnam.

Financial situation

LafargeHolcim made a net loss of US$1.46bn in 2017 from a revenue of US$23.4bn. In 2016 it made a US$1.92bn profit from a revenue of US$26.9bn. As it announced this unfavourable set of results the group drew attention to its new ‘Strategy 2022 - Building for Growth.’ The strategy aims to drive profitable growth and simplify the business to deliver resilient returns and attractive value to stakeholders.

LafargeHolcim says that the new strategy will shift gears towards growth of both the top and bottom line over the next five years. It targets annual net sales growth of 3-5%, annual recurring earnings before interest, tax, depreciation and amortisation (EBITDA) growth of at least 5%, improvement in free cashflow to over 40% of recurring EBITDA and an 8% improvement in return on invested capital (ROIC).

In the first quarter of 2018, LafargeHolcim saw falling earnings, which it blamed on poor weather in North America and Europe. Its recurring earnings before interest, taxation, depreciation and amortisation (EBITDA) fell by 7.7% on a like-for-like basis year-on-year to Euro587m from Euro678m in the same period of 2017. Its net sales rose by 3.1% to Euro4.89bn and its cement sales volumes rose by 3.2% to 47.7Mt on a like-for-like basis.

By region cement sales volumes fell on a like-for-like basis in Europe, Middle East Africa and North America. LafargeHolcim said that cement volumes were down slightly in its Middle East Africa region due to a mixed outlook in the region with ‘challenging’ conditions in key markets. In Asia Pacific it said that China and India drove its growth in sales and profits but that there was continued pressure in South East Asia.

Recent news

In May 2018 LafargeHolcim was accused of crimes against humanity by the European Center for Constitutional and Human Rights (ECCHR) and Sherpa, two non-governmental organisations, over the former Lafarge Syria’s conduct in Syria in 2012-2014. It has been accused of paying armed groups, including Islamic State, US$5.6m to help keep its plant open during the Syrian conflict and numerous executives have been detained. These include the former head of security for Lafarge Syria and LafargeHolcim’s head of human resources. Former LafargeHolcim CEO Eric Olsen resigned to clear the air over the matter, despite claiming no involvement. Bruno Lafont, the former head of Lafarge, was also questioned.

In May 2018 LafargeHolcim announced that it would be closing its main Paris building, the site of the former Lafarge headquarters, by the end of 2018.

“This painful but necessary simplification step is key to creating a leaner, faster and more competitive LafargeHolcim,” said chief executive officer Jan Jenisch. The move follows decisions to close offices in Singapore and Miami, USA.

3. Anhui Conch

Anhui Conch was founded in 1997 and grew rapidly as China’s cement consumption rose in the early 2000s. Like other Chinese producers, it has recently been forced to adjust to falling demand, although higher prices resulted in a 35% year-on-year increase in revenue in 2017.

| HQ | China | 2017 Cement Sales | 290Mt |

| Capacity | 335Mt/yr | 2017 Revenue | US$11.9bn |

Anhui Conch is the third-largest cement company in 2018. In its 2017 Annual Report the group said that it had clinker and cement production capacities of 246Mt/yr and 335Mt/yr respectively. During the year Anhui Conch opened eight cement grinding plants in China, including Quanjiao Conch Cement, Anhui Xuancheng Conch Cement and Nantong

Conch Cement.

Outside of China the company completed phase two of its Merak grinding plant in Indonesia. It also finished building and started cement production at its North Sulawesi Conch plant in Indonesia and its Battambang Conch plant in Cambodia. The units in Indonesia and Cambodia are due to start commercial production during 2018. A new plant, Luang Prabang Conch, is being built in Laos and preliminary work on projects at Volga Conch in Russia, Vientiane in Laos and Mandalay in Myanmar is underway.

During 2017 Anhui Conch sold 295Mt of cement and clinker, a year-on-year increase of 6.6%. This represents a capacity utilisation rate of 88%.

Financial situation

Anhui Conch’s sales revenue grew by 35% year-on-year to US$11.9bn in 2017 from US$8.85bn in 2016. Its net profit nearly doubled to US$2.51bn from US$1.36bn. The cement producer said that it had ‘seized the favourable opportunities arising from the state’s further deepening of supply-side structural reform and the promotion of off-peak season production.’

In the first quarter of 2018, Anhui Conch Cement’s sales revenue rose by 38% year-on-year to US$2.98bn from US$2.16bn in the same period of 2017. Its net profit more than doubled to US$757m from US$341m. The rise in sales and profits has been attributed to rising cement prices in smaller cities and demand from the Xiongan New Area project. The cement producer also said that it received a government subsidy of US$18m.

Recent news

In March 2018 Anhui Conch reported that it had spent over US$7.9m on a 50,000t CO2 capture and purification pilot project at its Baimashan cement plant in Anhui province. The unit was scheduled to begin operation in the first half of 2018. The group has started the project in order to participate in the government’s ‘Intended Nationally Determined Contributions’ CO2 emission reduction initiative.

Also in June 2108, Anhui Conch suspended production at three of its production lines at the cement plant run by its Tongling Conch subsidiary at Gusheng in Anhui province. The suspension has followed the temporary closure of a pier used by the plant in late May 2018, in accordance with new government regulations on drinking water supply and pollution.

Use of the pier has been suspended as it is close to the Tongling Water Treatment Plant. The pier had been used to export cement and clinker products from the unit and bring in raw materials such as coal. The temporary suspension of the plant’s production lines has reduced its clinker production capacity to just under 9Mt/yr from 15Mt/yr.

In April 2018 Anhui Conch announced plans to open an office in Tunis, Tunisia to explore investment opportunities within north Africa.

In June 2018 it was announced that Anhui Conch was discussing the possibility of building a cement plant in Odessa, Ukraine, as part of a possible larger commercial and industrial park.

In December 2017 Anhui Conch signed a strategic cooperation agreement with China Railway Materials Trading, a subsidiary of China Railway Group.

Yu Shui, the assistant general manager of Anhui Conch, and Xiao Song, deputy general manager of China Railway Materials Trade Group, signed the agreement. Anhui Conch plans to establish a supply chain agreement with the state-owned company.

4. HeidelbergCement

Germany-based HeidelbergCement rose up the global cement capacity rankings in 2016 when it acquired Italian rival Italcementi. It has been bolstered by its new assets and has only had to sell a very few plants due to competition issues.

| HQ | Germany | 2017 Cement Sales | 126Mt |

| Capacity | 187.8Mt/yr | 2017 Revenue | US$20.2bn |

HeidelbergCement continued to benefit from its 2016 acquisition of Italy’s Italcementi in 2017. Its sales revenue rose by 2.1% year-on-year on a like-for-like basis to Euro17.3bn in 2017 from Euro17.1m in 2016. Its cement sales volumes increased by 1.1% to 126Mt from 124Mt.

“The challenges were numerous: energy cost inflation, increased competition in emerging markets, especially in Indonesia, uncertainties following the Brexit decision and bad weather, especially in the USA,” said Bernd Scheifele, chairman of the managing board of HeidelbergCement. “Nevertheless, we were able to increase our result from current operations as guided. The consistent focus on efficiency and margin improvement and the successful integration of Italcementi that led to higher than expected synergies contributed to this success. Overall, 2017 was a record year for sales volumes, revenue and results from current operations.”

The group reported increasing cement deliveries in all areas except Africa-Eastern Mediterranean in its preliminary results. In this region cement sales volumes fell by 0.6% to 19Mt from 19.1Mt due to a poor market in Egypt. Otherwise it described its market development in the region as ‘varied.’

HeidelbergCement also increased its cement sales volumes in the first quarter of 2018, despite facing poor weather and coping with reduced working days. Sales volumes of cement rose by 2% year-on-year to 28.2Mt from 27.5Mt in the same period of 2017. Falling sales volumes in Europe and North America were offset by growth in Asia-Pacific and Africa-Eastern Mediterranean Basin. In Asia, Indonesia and India contributed strongly to its growth. In Africa, increases in sales volumes were recorded in Egypt, Ghana and Tanzania. Its sales revenue increased on a like-for-like basis by 2% to Euro3.78bn.

Recent news

HeidelbergCement completed its acquisition of Cementir Italia from Cementir Holding in Italy during 2017, via its Italcementi subsidiary. It offloaded the Maddaloni plant due to competition issues in June 2018, selling it to local producer Colacem.

In February 2018 HeidelbergCement announced that its subsidiary Lehigh Cement Company had signed an agreement to sell its 51% position in Lehigh White Cement Company to the minority shareholders Aalborg Cement Company and Cemex. “As a niche product with small volumes, the standalone production of white cement does not fit the strategic focus on efficiency of HeidelbergCement,” said

Bernd Scheifele.

HeidelbergCement hosted a ground breaking ceremony for the Calix carbon capture pilot at CBR’s cement plant at Lixhe on 7-8 February 2018. The ceremony itself took place at the Liège Oupeye Water Treatment Plant near Liège as part of the inaugural Innovation in Industrial Carbon Capture Conference.

Work on a grinding plant upgrade by HeidelbergCement’s subsidiary Cimburkina in Burkina Faso started in February 2018. This will double the plant’s capacity from 1Mt/yr to 2Mt/yr.

In January 2018 HeidelbergCement’s Ghanaian subsidiary Ghacem opened a new 3000t terminal at Sefwi Dwenase in Sefwi-Wiawso Municipality. The unit is the cement producer’s sixth terminal in Ghana.

Cementa, the Swedish subsidiary of HeidelbergCement, applied for an extension to its limestone mining lease at its Degerhamn cement plant in December 2017. The current lease expires in 2022. The renewal covers 15Mt for an additional 30 years.

In November 2017 HeidelbergCement’s Egyptian subsidiaries Suez Cement and Helwan Cement agreed merger terms. The group also sold 50% of the voting rights in its Georgian businesses to Cement Invest in the same month.

5. Cemex

Mexico’s Cemex increased its cement capacity marginally in 2017, bringing to an end an extended period of contraction brought about by debt and the global financial crisis. CEO Fernando González stated in March 2018 that Cemex was considering acquisitions in Brazil and India, two major cement markets from which it is currently absent.

| HQ | Mexico | 2017 Cement Sales | 68.5Mt |

| Capacity | 95.6Mt/yr | 2017 Revenue | US$2.57bn |

The modern-day Cementos Mexicanos (Cemex)can trace its history back to 1906 and the founding of Cementos Hidalgo in northern Mexico. It merged with Cementos Portland Monterrey, renaming as Cemex in 1931. It expanded to Spanish-speaking nations, including Spain, Venezuela, Panama, Colombia, the Dominican Republic and Costa Rica in the 1990s, as well as Egypt, the US and the Philippines. In the 2000s expansion continued into Europe via the acquisition of RMC (2003), as well as Thailand (2001) and Puerto Rico (2002). It gained further assets through the acquisition of Australia’s Rinker in 2007. In 2018 Cemex is the fifth-largest global cement producer, with 95.6Mt/yr of cement production capacity.

Financial situation

Cemex’s operating earnings fell in 2017 due to a lower contribution from the US and South America, despite growth in Mexico and Europe. Its operating earnings before interest, taxation, depreciation and amortisation (EBITDA) fell by 7% year-on-year to US$2.57bn in 2017 from US$2.75bn in 2016.

Cemex’s net sales grew by 2% to US$13.7bn from US$13.4bn and its cement sales volumes remained stable at 68.5Mt. The cement producer also reported an unexpected loss in net income of US$105m in the fourth quarter of the year, which it blamed on taxes and other costs.

“Although 2017 was a challenging year… We had important headwinds during the year: underperformance in Colombia, Egypt and the Philippines as well as increased energy costs, mainly in Mexico. As we have done in the past, we focused on the variables we control to dampen these headwinds and we continued to deliver solid results,” said Fernando A Gonzalez, Chief Executive Officer (CEO) of Cemex.

Cemex’s first quarter operating earnings for 2018 also fell due to poor weather and fewer business days. Its operating earnings before interest, taxation, depreciation and amortisation (EBITDA) fell by 4% year-on-year to US$535m for the period from US$557m in the same period in 2016. Its new sales rose by 8% to US$3.38bn from US$3.14bn and its cement sales volumes rose slightly to 16.1Mt from 15.9Mt.

Recent news

In June 2018 Cemex UK announced that it would move its headquarters from Thorpe, Surrey to its offices in Rugby, Warwickshire, effective 1 July 2018. The new premises were the former global head offices for the Rugby Group until 2000.

Also in June 2018, Cemex announced that its Cemex Go digital platform had reached more than 10,000 users. The system allows the company and its customers to manage order placement, live tracking of shipments and invoices and payments for the company’s main products, in real time.

Cemex Philippines has committed up to US$57m in 2018 towards the construction a new production line at its Solid Cement plant in Antipolo, Rizal. The project will increase the plant’s production capacity to 3.4Mt/yr from 1.9Mt/yr.

Cemex Latam signed an agreement to sell its stake in Cimento Vencemos do Amazonas to Votorantim Cimentos for US$30m in May 2018.

In March 2018 Cemex announced that it had become the first company in the cement industry to successfully operate plants by remote control, from its central location in Monterrey, Nuevo León.

According to the company, the Cemento Control Center (C3) operates 365 days a year, tracking live data from the operation of 14 cement plants, 25 kilns and 86 mills in Mexico. It also monitors a cement plant in Colombia and another in the US.

6. Ultratech Cement

India’s largest cement producer grew during 2017 by purchasing Century Textiles and Industries (12.4Mt/yr) and assets from Jaiprakash Associates (18.7Mt/yr). It commissioned a 2.5Mt/yr plant during 2017 and is also trying to acquire Binani Cement (11.3Mt/yr).

| HQ | India | Cement Sales (Year 31 March 2018) | 59.3Mt |

| Capacity | 93.5Mt/yr | Revenue (Year to 31 March 2018) | US$4.4bn |

7. China Resources Cement

China Resources Cement runs 45 clinker lines and 95 grinding plants across seven Provinces in China. One clinker line and two of the grinding plants were commissioned in 2017.

| HQ | China | 2017 Cement Sales | 75.9Mt |

| Capacity | 83.3Mt/yr | 2017 Revenue | US$3.8bn |

8. Votorantim

Votorantim Cimentos is one of the most international Brazilian cement producers, with capacity interests in North and South America, India, Turkey, Spain and Tunisia.

| HQ | Brazil | Capacity | 70.9Mt/yr | 2017 Revenue | US$2.5bn |

9. Taiwan Cement

Taiwan Cement was established in 1946. It is the seventh-largest cement producer in 2018, with 69Mt/yr of cement capacity in Taiwan and China.10. CRHCRH acquired numerous cement production assets in North America and Europe in 2017 to add to those it bought from the fallout of the LafargeHolcim merger in 2015 and further purchases in 2016.

| HQ | China | Capacity | 69.0Mt/yr | 2017 Revenue | US$870m |

10. CRH

CRH acquired numerous cement production assets in North America and Europe in 2017 to add to those it bought from the fallout of the LafargeHolcim merger in 2015 and further purchases in 2016.

| HQ | Ireland | Capacity | 63.3Mt/yr | 2017 Revenue | US$29.4bn |