This regional report looks at eight contiguous EU Member States that were formerly part of the Eastern Bloc: Bulgaria, Croatia, Czechia, Hungary, Poland, Romania, Slovakia and Slovenia. The three Baltic EU states, Estonia, Latvia and Lithuania will be covered separately in a future issue.

The eight countries covered by this article share 56.7Mt/yr of integrated cement capacity and are home to around 96.8 million people. Cement production is dominated to the tune of 85% by well-established multinational cement producers, including HeidelbergCement, LafargeHolcim and Cemex. Smaller multinationals are also present. This is a legacy of a rapid rush towards privatisation by these countries (and many others) after the collapse of communism in the early 1990s. Many plants, formerly state-owned enterprises, were extensively renovated and western European working practices, including the use of alternative fuels, were introduced to these ‘new’ markets.

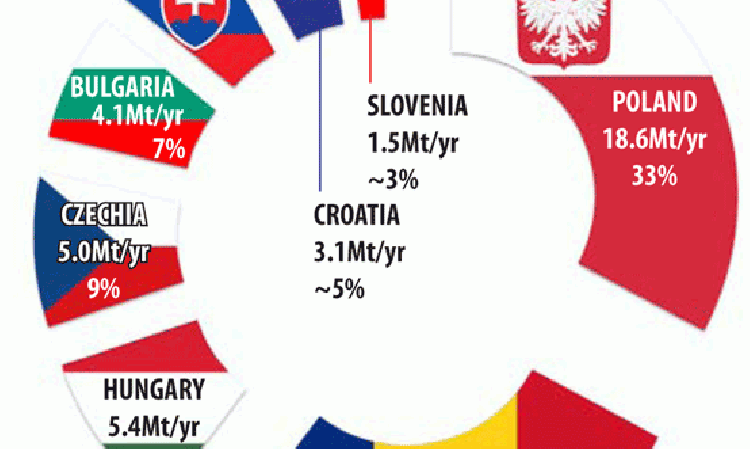

The leading companies’ integrated cement capacities can be seen in Table 1, and Figure 1 shows the eight countries’ installed integrated cement capacity. By far the largest national cement sector is that of Poland, which has around 18.6Mt/yr (33% of the group’s capacity). The smallest is Slovenia, with just 1.5Mt/yr (~3%).

| Company | Capacity (Mt/yr) | Share (%) |

| HeidelbergCement | 16.5 | 29.1 |

| LafargeHolcim | 13.2 | 23.2 |

| CRH | 9.1 | 16 |

| Cemex | 6.1 | 10.9 |

| Buzzi Unicem | 2 | 3.5 |

| Titan Cement | 1.5 | 2.7 |

| Others | 8.3 | 14.6 |

Above - Table 1: The largest cement producers in Central and Eastern Europe are all multinational producers. Source: Global Cement Directory 2019.

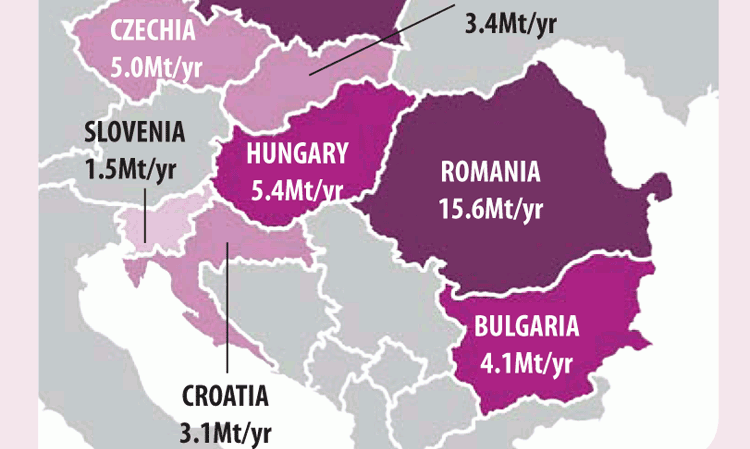

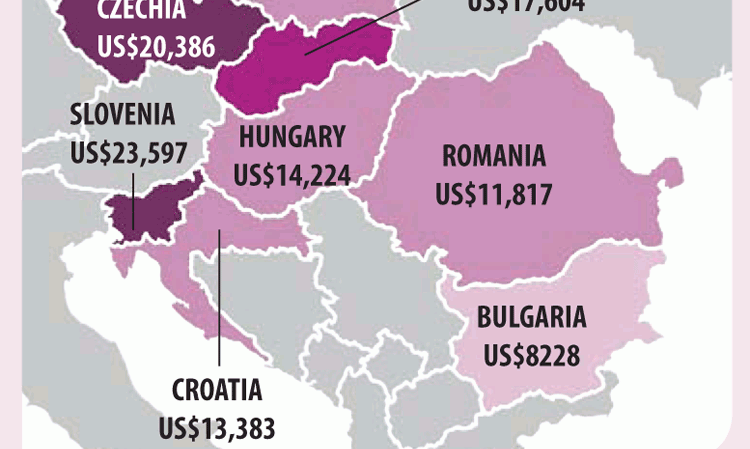

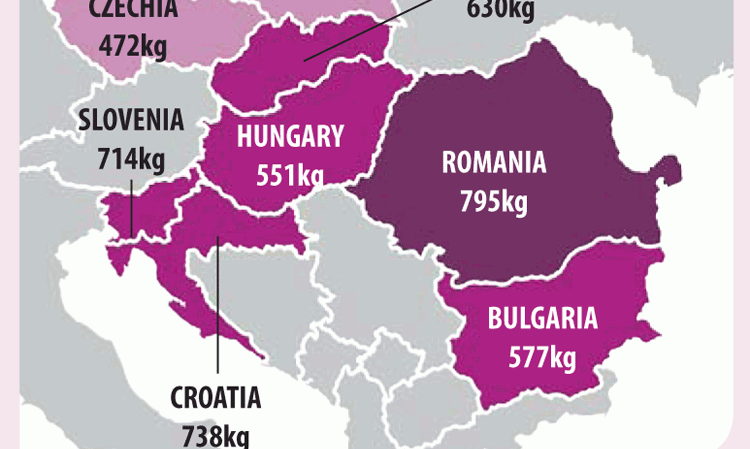

Figures 2 - 4 show the relative cement capacities, GDP/capita and cement capacity/population for each country. While capacities and GDP/capita values are quite varied, there is less variation in cement capacity/population data. This metric generally increases from north west to south east within this group of eight countries.

Bulgaria

Bulgaria is situated in south east Europe to the west of the Black Sea. It borders Romania, Turkey, Greece, North Macedonia and Serbia, neighbours with which it has had numerous territorial disputes over the years.

After nearly 500 years of Ottoman rule, Bulgaria secured independence with the help of Russia in 1878. It was part of the Central powers during the First World War and reluctantly provided assistance to the Axis from 1941 to 1944 during the Second World War. Bulgaria subsequently became a socialist republic with policies aligned with those of the Soviet Union.

After a shift towards the political centre by the ruling party in the late 1980s, the first multi-party elections for 60 years were held in 1991. During the 1990s Bulgaria experienced economic hardship as its inefficient industries were exposed by market realities. Following much readjustment, it was able to join the EU on 1 January 2007.

Cement sector

Bulgaria has four cement plants, all of which are operated by three major multinationals: HeidelbergCement, LafargeHolcim and Titan Group. Three integrated plants share a capacity of 4.1Mt/yr and a single 0.5Mt/yr grinding plant brings the national total to 4.6Mt/yr.

The German cement multinational HeidelbergCement is the country’s largest cement maker by installed capacity. It is active in Bulgaria via two subsidiaries. The larger is Devnya Cement, which operates a 1.5Mt/yr plant in Devnya. Vulkan EAD operates a 0.5Mt/yr plant in Dimitrovgrad.

The plant at Devnya was established by the Bulgarian government in 1954 and opened in 1958. It saw a series of expansions through the 1960s and 1970s, with four wet process kilns in operation by the close of the 1980s. Italcementi bought the company in 1998 as part of Bulgaria’s privatisation drive. The new owner provided significant investment in the plant before embarking on a major upgrade in 2012. By 2015, a new 1.5Mt/yr dry process line had been installed by China’s Sinoma to replace the outdated wet process kilns. In 2016, ownership of the plant passed to HeidelbergCement when the multinational acquired the entirety of Italcementi.

Vulkan EAD traces its history back to 1940 when construction began on a two kiln plant at Dimitrovgrad. The first line produced its first cement in 1947, with the second joining it a year later. Two further kilns were added in 1953 and 1965. As with Devnya Cement, Vulkan EAD was acquired by Italcementi in 1999. Investment followed before Italcementi was bought by HeidelbergCement in 2016. The facility now operates as a grinding plant only.

The second-largest player in the Bulgarian cement sector is the Greek multinational Titan Cement. It is active via its subsidiary Zlatna Panega Cement. Zlatna Panega was established by Italian investors in 1907 during a period of great expansion in Bulgaria’s cities. The plant operated until 1966 when it moved to its current site with five new wet process kilns. Zlatna Panega Cement was acquired by HeidelbergCement in 1998, which subsequently sold it to Titan Cement in 2004. Titan extensively upgraded the plant, which now operates two dry process lines that share a capacity of 1.5Mt/yr. Zlatna Panega Cement reported that it sold 0.57Mt of cement within Bulgaria in 2017, the latest year for which it has released data. It additionally exported 0.11Mt of clinker.

The Swiss multinational LafargeHolcim is present in Bulgaria via Holcim Bulgaria, which operates a 1.1Mt/yr integrated plant in Beli Izvor. The plant was established in 1960 and was privatised by Holcim in 1997. Holcim invested around Euro147m in the plant, taking the capacity from 0.35Mt to 0.8Mt in 2006 and then to 1.1Mt/yr in 2008.

Croatia

The Republic of Croatia is located in south east Europe and shares land borders with Slovenia, Hungary, Serbia, Bosnia & Herzegovina and Montenegro. The country occupies the vast majority of the northern coastline of the Adriatic Sea.

Formerly allied to Austria-Hungary until 1918, Croatia became part of the Kingdom of Yugoslavia in 1918 before a brief spell of independence during the Second World War. It then became a unit of the Socialist Federal Republic of Yugoslavia until 1991, when it declared independence. This goal was achieved in 1995, but only after a fierce war with the Yugoslav army.

Since independence, Croatia has witnessed rapid development. Its GDP has increased by a factor of 2.5 between 1996 (US$22bn) and 2017 (US$55bn), with a peak of US$70bn in 2008. The country joined the EU as a full Member State on 1 January 2013 after an eight year application process.

Cement sector

Croatia has five integrated cement plants as of 2019 that share a capacity of 3.1Mt/yr. Four of the plants are operated by multinational players (2.5Mt/yr, 81% of capacity), with a single local producer (0.6Mt/yr, 19%). The country has no grinding-only plants.

The largest producer of cement in Croatia is Cemex Hrvatska, which owns three of the five plants. It has an installed capacity of 2.0Mt/yr, around 65% of the national capacity. It entered the market in 2005 when it acquired the entire assets of UK-based cement maker RMC Group.

The largest is Cemex’s Sv Juraj plant, which began operations in 1912. It has a 3100t/day (1Mt/yr) Polysius Dopol kiln that dates from 1979. The kiln has a four-stage preheater and a riser duct, but no precalciner. It has a 70m-long Claudius Peters grate cooler with a high-efficiency static part to improve thermal efficiency, which was installed in 2003. Sv Juraj also has a 235t/hr raw mill and two 120t/hr cement mills. There are four cement silos, each with 12,500t of capacity. The plant is the only one of Cemex Hrvatska’s sites that has bagging facilities. It has two palletisers, one by Beumer Group and one by Möllers Group. As such, 6600t/day of bulk cement can be dispatched by ship or truck and 3000t/day of bagged cement can be dispatched by truck, train or ship. 2640t/day of big-bag clinker can be dispatched by ship, truck or train and 5000t/day of bulk clinker can be sent by ship or truck.

Cemex’s Sv Kajo site began operations in 1904. The plant has a 1400t/day (0.5Mt/yr) KHD four-stage preheater kiln with no calciner, one main burner and a Claudius Peters grate cooler. The site also has a 120t/hr raw mill, a 70t/hr cement mill and four cement silos, each with a 6000t capacity. Up to 4500t/day of cement can be shipped in bulk from the site by truck, train or ship, while 3000t/day of clinker can be dispatched in bulk by truck.

Cemex’s Sv 10 Kolovoz site began operations in 1908. It is Cemex Hrvatska’s smallest cement plant and is currently mothballed due to poor market demand. It has a 1180t/day (0.4Mt/yr) KHD four-stage preheater kiln with no calciner, one main burner and a Claudius Peters grate cooler.

The second-largest cement producer in the Croatian market is Nasicecement, part of Nexe Group. It operates a 0.6Mt/yr integrated plant that has been in operation since 1975.

The third and final player is Holcim Hrvatska, a member of LafargeHolcim, which operates a 0.5Mt/yr plant in Koromačno, Istria. The plant has been in operation since 1926.

Czech Repulic

Located in the very centre of Europe, the land currently occupied by Czech Republic has a long and complex history, variously under the control of Slavs, Austria-Hungary and the Kingdom of Bohemia. In 1918 the Kingdom of Bohemia ceased to exist, its territory merging instead with Slovakia and Carpathian Ruthenia (now mainly part of Ukraine). The new entity, Czechoslovakia, existed in various forms from 1918 until 1992. It was under Communist rule as part of the eastern bloc between 1948 and 1989. Czechoslovakia subsequently governed itself as a democracy for three years. However, calls for greater autonomy from Slovakia led to near-continuous deadlock in its Parliament. In 1992 it was decided that two halves should go their separate ways as of 1 January 1993, although political wranglings nearly jeapordised the separation process. After separation, the Czech Republic joined the EU on 1 May 2004. It officially registered the snappier name ‘Czechia’ in July 2016.

Cement sector

There are six cement plants in Czechia, five of which are integrated. The integrated plants share a capacity of 5.0Mt/yr. The largest player is HeidelbergCement via its subsidiary Českomoravský Cement. The company operates two cement plants, at Mokrá and Radotín. Construction of the Radotín plant was permitted in 1871. Following significant upgrades and the nationalisation of the company in the 1950s, the decision was taken to rebuild the plant in 1959. It came online in 1961. HeidelbergCement entered the company as a joint stock partner in 1991.

The Mokrá plant had a difficult birth between 1957, when the first plans for a plant in the area were mooted, and 1968, when the first kilns were put into operation. It was privatised by Belgian firm CBR in 1991. Both plants, as well as a third at Malomerice (1907 - 1997) were brought under the Českomoravský Cement banner by HeidelbergCement in 1998.

Italy’s Buzzi Unicem is present in Czechia through its ownership of Cement Hranice. The Hranice plant was established in 1954 with a capacity of 0.11Mt/yr. This was significantly increased between 1987 and 1992 before acquisition by Dyckerhoff in 1997. The company and plant became part of Buzzi Unicem in 2004, when it took over the entirety of Dyckerhoff. It now has a capacity of 0.4Mt/yr.

LafargeHolcim operates a single 1.1Mt/yr plant in Czechia, at Čížkovice. The plant was established in 1898 with wet kilns but switched to dry production in 1910, highly unusual for the time. The plant was nationalised after the Second World War, with a new kiln installed in the 1970s. Lafarge entered the company in 1992, installing a new clinker cooler in 1995 and a preheater in 1997. The plant was absorbed into LafargeHolcim in 2015.

Mexican multinational Cemex is present in Czechia via its Prachovice integrated plant and Dětmarovice grinding plant. The cement plant at Prachovice has been making cement since 1955. It was set up as a state-run concern with three wet kilns that operated throughout the 1960s and 1970s. They had a combined capacity of 0.6Mt/yr. In 1980 the kilns were replaced by one 0.9Mt/yr dry process line with a preheater tower from the Czech state company PSP, now part of IKN. In 1990 the plant was partly privatised, with Holderbank (subsequently Holcim) the purchaser. Holcim operated the Prachovice plant until the end of 2014, when ownership was transferred to Cemex. This transaction was part of a wider asset swap between the two companies in Europe prior to the merger of Holcim and Lafarge.

Hungary

Hungary traces its history back to the settlement of the previously nomadic Magyars in Europe in the 10th Century. Its borders were pressurised over the centuries by external powers, notably the Ottomans. Hungary later became part of the Austro-Hungarian Empire. The dissolution of the Habsburg Monachy in 1918 led to a number of treaties that saw Hungary reduced to a third of its former size, with territories ceded to six of its neighbours. Some areas were regained by Hungary in the 1930s. During the Second World War, Hungary participated on the side of Nazi Germany, partly due to the offer of further territorial gains in the event of victory. Afterwards, Hungary was occupied by the Soviet Army and transitioned to communism. A popular uprising against the government in 1956 was crushed by Soviet forces and the country remained communist until 1989. The country joined the EU on 1 May 2004.

Cement sector

Hungary’s cement industry comprises six integrated facilities that share 5.4Mt/yr of cement capacity. As elsewhere in the region, they are predominantly owned by multinational producers, which account for 89% of capacity.

The largest producer is Duna Dráva Cement, a 50:50 joint-venture between HeidelbergCement and Schwenk Zement. It operates two 1.4Mt/yr cement plants at Beremend and Vác, giving it 2.8Mt/yr of capacity, 52% of the national total. The Beremend plant, active since 1910, has seen a number of upgrades over the years, most recently between 2007 and 2009. It has a capacity of 1.4Mt/yr. The Vác plant, active for over 50 years, underwent a Euro22m upgrade to reduce its airborne emissions in the two years to April 2018. Germany’s IKN modified the clinker line to handle a refuse-derived fuel (RDF) substitution rate of up to 100% in the calciner. The two lower cyclone stages were replaced, a complete new preheater tower with an inline calciner was erected and a new bypass system and a new static inlet in the clinker cooler were installed. IKN completed the project in just less than two years on an engineering, procurement, and construction (EPC) basis. Denmark’s FLSmidth also worked on the project replacing the line’s bag filters with an electrostatic precipitator system. This part of the environmental upgrade cost Euro4.7m. On 1 January 2019 Duna Dráva Cement acquired Readymix Hungária, doubling its concrete business line and significantly expanding its gravel mining activities.

The second-largest producer in the Hungarian market is Ireland’s CRH, which operates plants at Miskolc and Lábatlan. They share 1.0Mt/yr of capacity. CRH purchased the plants 2015 as part of a major acquisition of Holcim assets that had to be sold in order for the merger with Lafarge to be approved by the European Commission.

The third-largest player in the market is Nostra Cement, a joint venture between LafargeHolcim (70%) and Hungarian construction materials producer Strabag (30%). The 1.0Mt/yr plant is the youngest in Hungary. Constructed began in 2007 and first cement was produced on 18 July 2011. The final player in the market is BECEM, which operates a 0.6Mt/yr plant in Bélapátfalva.

Poland

Poland is both the largest and most populous country covered in this article. As other nations, it was at the crossroads of changing European boundaries for many hundreds of years. From its territorial peak in 1492, when it was the largest country in Europe as Poland-Lithuania, it gradually contracted, losing its territory altogether at the end of the 18th Century. The end of the First World War in 1918 led to the unexpected opportunity for the establishment of a Second Polish Republic. In 1939 Nazi Germany invaded Poland, the opening event of the Second World War. After occupation by Nazi and Russian forces, Poland regained control of its territory in 1945. The country was run under communist systems until 1989. It joined NATO a decade later and joined the EU in 2004.

Cement sector

As might be expected, the country with the largest population in this article also has the largest cement sector. There are 10 integrated cement plants that share a capacity of 18.6Mt/yr and three grinding plants with a capacity of more than 1.7Mt/yr. The Polish Cement Association stated that cement sales rose by 7% year-on-year to around 18Mt in 2017, the most recent year for which it has made data available. In April 2018, the Institute of Economic Forecasting and Analysis forecast that sales will grow by 8% in 2018 to 17.9Mt.

The largest cement producer by installed capacity in Poland is HeidelbergCement, which entered the Polish market in 1993. Today it operates a 4.0Mt/yr integrated plant at Opole via Górażdże Cement and a 1.4Mt/yr grinding plant at Katowice via Ekocem. The Górażdże plant is HeidelbergCement’s largest and most modern in Europe. The second-largest producer is LafargeHolcim via its two subsidiaries Lafarge Cement Polska (4.0Mt/yr, two integrated plants) and Cementownia Nowa Huta (0.3Mt/yr, one grinding plant). The third-largest producer is Cemex Poland. which operates two integrated plants and one grinding plant. The fourth-largest is CRH, via Grupa Ozarów (2.8Mt/yr, two integrated plants). It entered the Polish market, its first outside of its native Ireland, in 1995. The remainder of the country’s cement players include Dyckerhoff Polska and independent players Cementownia Warta and Cementownia Odra.

These players will be joined by a new grinding plant operator in the coming years. Cem’In’Eu is in the process of setting up a number of identical grinding plants with its supplier Intercem Engineering. Located at the Port of Gdynia, its plant in Poland, Pomorski Cement, will supply northern Poland in the area surrounding Gdansk.

Cement sector news

December 2018: Ernest Jelito, the president of Górażdże Cement, was elected as the chairman of the Polish Cement Association in December 2018. He began his new role at the start of 2019.

November 2018: LafargeHolcim Poland invested Euro2.5m to set up an automated laboratory in a new building at its Kujawy cement plant in November 2018. The laboratory is used to analyse the quality of raw meal, clinker and cement every hour over a 24 hour period. Results are then fed back to the control room to allow for production modifications.

July 2018: Lafarge Poland officially opened its new Siekierki ash separation plant in July 2018. The unit was developed with local power generation company PGNiG Termika. The plant uses technology from the US-based Separation Technologies, using its proprietry electrostatic process.

The unit converts fly ash into two products: ProAsh containing less than 5% flammable parts and HiCarbon fuel containing about 30 - 50% flammable parts. ProAsh ash is used as a construction product used in cement production, ready-mix concrete and prefabricated construction. HiCarbon is used as a fuel as it contains significant amounts of unburnt carbon.

Romania

Like much of the Balkans, Romania was variously occupied by the Romans, Ottomans and Austro-Hungarian forces for much of its history. In 1866, however, a coup gained it its independence. During the First World War, Romania spent two years on the sidelines, although it eventually joined the Allies in 1916. Between the World Wars, Romania grew to its largest territorial extent as a liberal constitutional monarchy. In the Second World War Romania once again attempted to remain neutral but its hand was forced, this time towards the Axis Powers. After the war, the country became communist, latterly under Nicolae Ceauşescu, who was executed in the Romanian Revolution of 1989. The economy had been thoroughly destroyed in the final years under Ceauşescu, making the transition to market economics in the 1990s particularly difficult. Romania became a member of the EU in 2007.

Cement sectorRomania has the second-largest cement sector among the eight countries reviewed here after Poland. Its nine cement plants, eight of which are integrated, possess more than 15.6Mt/yr of cement production capacity. There are just three producers, all multinationals. There are no cement producers native to Romania.

HeidelbergCement Romania is the largest player, with 7.2Mt/yr of capacity across three integrated cement plants, all of which are fairly large. This is sufficient to give the German company 46% of Romania’s cement capacity. HeidelbergCement entered the Romanian market in 1998 by acquiring Moldocim SA Bicaz’s plant in Taşca. It rapidly expanded its presence through the establishment of new strategic concrete plants. It bought its second plant in Romania, the Chişcădaga facility, in 2000. In 2002 it became a major shareholder in Romcif Fieni. It became the sole shareholder of the plant in 2016.

The second-largest cement producer is LafargeHolcim via Holcim Romania. Like HeidelbergCement, it operates three integrated plants. They share a capacity of 5.3Mt/yr, enough to give LafargeHolcim around 40% of Romanian capacity. The former Holcim entered the market in 1997.

The final player in Romania is CRH, which operates two integrated plants (3.1Mt/yr) and a single grinding plant. CRH entered the Romanian cement market in 2015 when Lafarge was forced by the European Commission to sell its assets as part of its merger with Holcim. However, CRH had previously been present in the country in other sectors.

Cement sector news

In November 2018 the Romanian Competition Council launched an investigation into an alleged anti-competitive agreement between the country’s three cement producers. It stated that it is concerned about possible coordination of prices between them since 2010.

As part of the probe, it conducted raids at the headquarters of the three companies and seized documentation. It has warned that fines of up to 10% of company turnover are applicable should it find any evidence of collusion. However, it also mentioned that companies that cooperated with the competition authority could expect leniency in the form of immunity to, or reduced, fines.

Slovakia

The history of Slovakia is very closely tied to that of neighbouring Czechia, variously under control of the Ottoman Turks, Austro-Hungarian Empire and other external forces over the centuries. Slovakia was a federal constituent within Czechoslovakia from 1918 until the start of 1993, when it separated from the Czech Republic after calls for greater autonomy. Following separation, Slovakia joined the EU on 1 May 2004.

Cement sector

Slovakia’s cement industry is the third-smallest among the eight nations in this group. Its four integrated cement plants share a combined 3.4Mt/yr of cement capacity. The country has no stand-alone grinding plants.

The largest producer is Ireland-based CRH, which operates the two largest plants. It has 1.9Mt/yr of capacity, around 56% of the country’s capacity. CRH entered the Slovak market in 2015 when it bought Holcim’s former assets in the country prior to the merger with Lafarge. While Lafarge does not have any assets in Slovakia, the European Commission viewed central Europe, in which there were many Lafarge and Holcim plants, in a wider context.

The 1.1Mt/yr Rohoznik plant is the larger of CRH’s two facilities. It traces its history back to 1971, although its first clinker was not made until 1976. It was privatised in 1992 when Holcim (as Holderbank) entered with an 84% stake. It added to the stake over the years, taking it to 99.7% by the time the plant was passed to CRH. Over the years the plant has undergone significant expansion. Recently it saw the installation of a Hotdisk combustion device for the burning of coarse alternative fuels from FLSmidth in 2005. It installed a ReduDust system from A TEC in 2013.

CRH’s other plant in Slovakia is the 0.8Mt/yr plant at Turňa nad Bodvou, which started production in 1974. It was privatised into Slovak hands in 1992, with German firm MF Beteiligungs GmbH taking the helm in 1999. Holcim acquired the plant in 2011. Holcim / Holderbank also had its hand in two further Slovak cement plants in the 1990s, both of which are now closed.

The second-largest cement producer in the Slovak market is Povazská Cementáren, which operates a 1.0Mt/yr plant in Ladce. The plant was first constructed in 1889 and began making cement in 1895. Zsolnauer Zement bought the plant in 1911 before it was acquired by the Hungarian General Credit Bank. The plant was brought under control of the government in 1950 and, in 1969, the plant was upgraded with a new rotary kiln. In 1971 the plant made 0.4Mt/yr for the first time. It was privatised in 1995 as an employee-led company, becoming Povazská Cementáren. It continued to expand its production rate in the 2000s, producing 1.0Mt for the first time in 2008.

The third and final producer of cement in Slovakia is Cemmac, which is owned by Hemag Holdings from neighbouring Austria. Hemag acquired the plant at Horné Srnie from the government when it was privatised in 1992. The plant itself traces its history back to 1929, when it had a clinker production capacity of just 100t/day. The plant underwent expansion with the addition of four new vertical shaft kilns. A fifth was added in 1968. The plant underwent a massive upgrade under Hemag in 1998, when a new 0.5Mt/yr dry process line with five stage preheater and calciner was installed.

Slovenia

Sandwiched between Austria to the north and Croatia in the south, Slovenia is the smallest country of those covered in this article. It also has the lowest population. It was part of the Holy Roman Empire, the Habsburg Monarchy and, more recently, part of Yugoslavia along with numerous other modern Balkan nations. It gained independence from Yugoslavia in 1991 and became a member of the EU on 1 May 2004.

Cement sector

In addition to the smallest area and population, Slovenia also has the smallest cement sector of the countries in this article. The country is home to just two integrated cement plants that share a capacity of 1.5Mt/yr.

The largest producer is Salonit Anhovo, which operates a 1.0Mt/yr plant in Anhovo, in the west of the country close to the Italian border. The plant celebrates its 100th Anniversary of business in 2019, having been established by Ivan Nibrant from Anhovo in 1919. The plant itself began production of cement on 2 May 1921. The plant operated with shaft kilns for the first 40 years, gaining a 350t/day wet process kiln in 1961 and a 2000t/day dry process line in 1977, at which point the wet kiln was closed. The plant made 1Mt of cement in a single year for the first time in 1986. In 2017 the plant began to use alternative fuels for the first time. In November 2018, Salonit Anhovo announced that it had spent Euro10m towards upgrades at the plant. Most of the funding went towards automation and environmental works. The work included the construction of new cement silos, the installation of devices to reduce NOx emissions, the purchase of new quarry machinery, measures to reduce noise levels and upgrades to the plant’s business information system. The company has also started to replace asbestos roofing on an old building and started demolishing disused buildings. These two last projects are valued at around Euro3m and are expected to be completed by the end of 2020.

The second producer in the Slovenian cement industry is LafargeHolcim, which operates the 0.5Mt/yr Trbovlje plant. The plant, formerly operated by Cementarnica Trbovlje, was acquired by Lafarge’s Austrian subsidiary Lafarge Perlmooser AG in 2002. It embarked on a significant renovation of the facility, making the plant one of the most advanced within Lafarge at the time. The plant was transferred to LafargeHolcim along with other former Lafarge assets as part of the merger between Lafarge and Holcim in 2015. In January 2018 the plant lost a legal battle to secure a revised environmental permit. It had wanted to increase its cement production capacity by using petcoke as a fuel.