The UK has long been a major player in the supply of waste-derived fuels for the cement industry, waste-to-energy sector and others applications within Europe. Here, Global Cement speaks with Andy Hill, Managing Director of Cynosure, about alternative fuels in the UK, the EU and further afield, as well as the future trends that will impact the market.

Global Cement (GC): Let’s start with a bit of background. Please could you outline your history in the waste-management / alternative fuels sector?

Andy Hill (AH): I started my career in the waste industry in the early 2000s with a company called Eco in the UK. It operated primarily in the realm of organic wastes and was very progressive in that it focussed on making quality products from the material it received. Eco was also one of the first to target biomass at the waste-to-energy sector, selling to combined heat and power generators in Sweden. From there I went to Suez, where I led the organics and alternative fuels business, which included wood, refuse-derived fuel (RDF) and solid recovered fuel (SRF), supplying to Europe, Scandinavia, Africa and India.

GC: What was your first contact with the cement sector?

AH: One of Suez’s Swedish wood clients came over to view one of Suez’s waste-processing facilities in the UK and there was a pile of what we considered to be ‘residual waste’ in the corner. He said he would like to take it in addition to the other fuels he was using. After some discussion, became clear to the Suez team that the material was in fact RDF. That was the genesis of RDF being marketed by Suez. At first we targeted the customers we already had, namely power plants in northern Europe. After a year, Suez was the largest UK exporter of RDF.

Shortly afterwards, we were approached by Neville Roberts from Cemex. He’d seen an opportunity to work with Suez to supply solid recovered fuel to Cemex’s Broceni plant in Latvia. A mobile line for SRF was built at one of Suez’s existing plants, which enabled a trial of 3000t. Cemex liked the quality and a longer contract then led to the development of Suez’s first full SRF production line in the UK.

As Suez developed the SRF side of its business, I was appointed chair of the steering committee for the group’s SRF activities. This gave me the opportunity to interact with colleagues from across Suez on the development of SRF globally. We shipped the first SRF from the UK to outside of the EU, to Morocco, Senegal and India. This developed a real passion of mine, namely developing opportunities for SRF in emerging markets.

GC: Is that the reason you established Cynosure?

AH: I founded Cynosure in April 2018. It brings stakeholders together to develop opportunities in markets in which waste-processing and alternative fuels are not common, using my expertise in supply chain development around the world.

What we find is that, in lots of places, there are significant challenges relating to stakeholder perception about alternative fuels and ‘burning wastes,’ so local ‘buy-in’ is crucial. What Cynosure does is put together the right expertise, contacts and local stakeholders to come up with optimum supply chain solutions for all involved. When you get it right, it’s very rewarding.

We have to view SRF as an engineered fuel product and have to work with local interests to put that position forward in some emerging markets. We have to make the link away from ‘waste’ towards a replacement for fossil fuels. If a firm does want to import SRF to an emerging market, it should contribute to the local situation and help develop local waste management infrastructure, be it relating to reception, transit, feeding or, indeed, production of SRF. A lot of countries could benefit from the knowledge developed by SRF producers.

GC: What are you working on right now?

AH: Right now I’m ‘flat out’ on a range of projects, including in the Bahamas, South America and the Middle East. Around 60-70% of my ‘run-time’ is dedicated to SRF and the cement sector, with biomass taking around 25 - 35% and the balance my non-executive roles. On the cement side, I am a Senior Advisor for N+P, a well-known Dutch producer of RDF, SRF and pelletised fuels.

There are some longer-term projects too. For example, I have a venture with some partners in Wales, UK, to set up our own SRF production facility. I’ve also set up some partnerships regarding biomass supply in Portugal and the Caribbean. Biomass is rising up in importance at the moment.

UK focus

GC: Is SRF a commodity...?

AH: SRF isn’t a commodity... yet. Firstly, commodities are consistent in terms of quality against a specification. Cement plants are generally looking for the same requirements, for example 16-18MJ/kg, <15% moisture, <0.8% chloride and so on. At present, some SRF producers face challenges to consistently meet some of these requirements. This is, in part, due to the downward price pressure put on SRF producers by cement manufacturers. The price pressure makes it difficult for SRF producers to invest in their facilities to actually make more consistent SRF. There needs to be a rebalancing of the sector towards long-term stability in supply and away from short-term price-based thinking.

A second point is that commodities have a fairly even balance between supply and demand. This is not the case at the moment for SRF. Eventually, I think this will be the case. If the rest of the world catches up with Europe on thermal substitution rate, that would be a game-changer and SRF would be in much greater demand, enough to call it a proper commodity. Think back to petcoke. In the early 1990s it was given away or refineries even paid to get rid of it. Now it is a valuable commodity.

GC: Let’s focus on the UK market. Can you outline the current dynamic in SRF supply and demand?

AH: While it is quite small in global terms, the UK cement sector is well developed in terms of its alternative fuel use. All plants are at an alternative fuel thermal substitution rate of at least 40 - 50%, with some exceptions up to 70 - 80%. They use SRF, tyre-derived fuel (TDF), hazardous liquids and other alternative fuels.

That said, the easiest gains have now been made by UK cement players, and the thermal substitution rate has been fairly static for a number of years. Further gains require significant investment. On the waste management side, the UK generates far more waste than it has landfill, recycling and alternative fuel capacity combined. Quite simply, that’s why the UK exports and has become a leading force in Europe in terms of RDF and SRF exports.

GC: Can UK cement producers get hold of the right types of SRF and other materials?

AH: At present, the UK’s cement players are able to secure enough of the right kind of material. There’s plenty of SRF feedstock, although some further processing facilities would certainly be useful. The trend right now is actually towards more material staying in the UK, as China has introduced new restrictions on the kinds of recyclable materials that it will import. Other Asian countries are now following suit and that’s causing a lot of material, particularly plastics and paper, to ‘back up’ into Europe as a whole. In the short-term, it’s good for the cement sector, as it is driving up fuel quality and raising energy values. At the same time they are also putting price pressure on SRF producers.

GC: The UK is clearly swamped with waste. What would be the best way to use or eliminate it?

AH: There needs to be contributions from across the waste heirarchy. This includes, in descending order of preference: Reducing the amount of waste generated; Re-using materials as they have been produced/used; Recycling waste that cannot be reused; Recovery of energy (waste-to-energy, alternative fuels) from non-recyclables, and; Disposal. The latest addition to the waste-heirarchy above re-use is for the public to Refuse packaging to drive producers to eliminate the waste that their products generate. There is currently a lot going on in the EU as a whole regarding extended producer responsibility for packaging and wider cultural awareness of disposable plastics. This is, in part, driven by reducing landfill capacity in the UK, which will run out over the next 5-10 years.

GC: What kind of reduction could refusing, reducing and re-using waste have to the amount of waste generated and, by extension, SRF stocks?

AH: That’s a hard question and I would not like to put a figure on it. There are so many dynamics at play. It will be interesting to see the effects of new legislation.

Talking exports

GC: How important is the UK to Europe-wide alternative fuel supplies?

AH: The UK ‘stole a march’ on other EU Member States in the early 2000s. It currently exports around 3Mt/yr of alternative fuels, including RDF. Of that amount, around 12 - 15% is SRF, so the amount exported in 2018 was around 350,000t.

In recent years there has been a gradual increase in the amount of SRF leaving the UK for Europe and elsewhere. However, a lot of material also stays at home. This is especially true at the moment with the uncertainty surrounding Brexit (the UK’s departure from the EU). SRF suppliers, particularly from France and Italy, are approaching the clients traditionally served by the UK-based exports. A lot of SRF users in the EU are rightly asking questions about whether or not UK companies will reliably be able to supply them after Brexit. French and Italian suppliers are not subject to those questions and are increasingly attractive, especially as Brexit drags on, which just creates uncertainty for both importers and exporters.

GC: How else has the prospect of Brexit, and in particular delays to Brexit, affected SRF producers and users in the UK?

AH: At present the UK has now ‘failed to leave’ the EU on two occasions, 29 March 2019 and 12 April 2019. This has affected a number of industries. A common example is when companies have ordered larger quantities of raw materials, parts, or whatever they need from Europe, in anticipation of disruption to their supply chain. However, all that’s happening at the moment is that they now have too much stock, costing them space in a warehouse, and cashflow issues.

For waste handlers, processors and exporters this is the case too, but in reverse. They want to get material out of the UK. However, the unusual thing about the waste processing sector is that they are generally contracted to receive waste over long periods. The waste keeps coming. They can’t phone up the municipality and say ‘not today thank you!’ Pressure builds up in the supply chain.

GC: What’s your take on the likely post-Brexit situation for the UK / EU SRF supplies?

AH: As I understand it, from my position as Chairman of the Wood Recyclers Association (WRA), the government and Civil Service have actually done a very good job to ensure that Trans-Frontier Shipment (TFS) permits will continue as at present after Brexit, whatever form that may take. They have engaged with the receiving country’s authorities and have agreed that there will be business-as-usual.

That said, there are practical considerations around the ports that nobody can really say much about until after Brexit actually happens. Will there be enough trucks coming and going? Will they be waiting at the dockside for 24-48 hours to cross the Channel rather than 1 - 3 hours at present? Will there be delays to ships?

I’d certainly like to think that the government, or indeed any future government, would dynamically seek to minimise disruption at the point of Brexit. To not do so would be to jeapordise the UK economy and would be very damaging to whichever political party that presided over the transition.

What about the ETS?

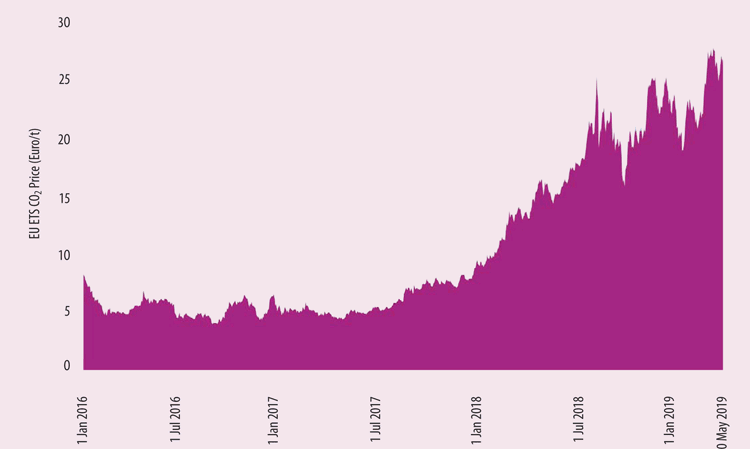

GC: How does the EU Emisions Trading Scheme (ETS) and recently increasing CO2 price affect alternative fuel trends in Europe?

AH: The EU ETS is now, after nearly 15 years, taking effect in the way it was designed to: Reducing CO2 emissions from industry. Anecdotally, I’m hearing that the EU cement sector becomes vulnerable to imports from outside Europe at a CO2 emission price of around Euro20/t. At present it is routinely Euro20 - 25/t. Indeed, it hit Euro27.24/t on 11 April 2019. The European Commission (EC) stated that it would implement import taxes to counteract the possibility of ‘carbon leakage’ but that has not yet transpired.

Historically, EU cement plants could rely on the over-allocation of permits. During the economic downturn some even made windfall profits by selling them. However, the reduction in the number of available permits is directly behind the CO2 price rise. The price is going to remain volatile, but it will most likely remain in the Euro15 - 20/t zone. To mitigate, producers must head towards alternative fuels and waste heat recovery. Biomass in particular has an important role to play, as it is effectively CO2-neutral. The CO2 emitted upon combustion is that which was absorbed as the biomass grew.

There’s another facet of the EU ETS that not so many people are aware of. EU-based cement companies can register their plants that don’t come under the jurisdiction of the EU ETS. This means that, if they reduce CO2 emissions in the registered plant, they can claim the CO2 credits for use in the ETS, as if the registered plant was in the EU. It effectively means ‘expanding the border’ of the EU ETS and encourages CO2 mitigation outside of the EU as well as inside it. This is an interesting dynamic for the future.

GC: How will supply and demand for alternative fuels in the EU change in the next 1-2 years?

AH: That’s an expansive question, so I suggest we break Europe down into ‘North’ and ‘South.’ In general Northern Europe has high use of alternative fuels (65 - 80% TSR or more) and there is relatively little that can be done to increase that without significant investment. Going forward, the benefit to Northern European plants will come from increased supply of better quality fuels due to China and the Far East import bans. They will be able to be more selective with the alternative fuels they use.

There are some complicating factors however. In Germany for example, all recyclable household waste is collected under the Yellow Bag scheme. That waste cannot be incinerated by law, be it in an energy-to-waste plant, cement kiln or anywhere else. Schemes like that, if adopted widely across Europe, might shift the boundaries on what is available to produce SRF.

Southern Europe generally has thermal substitution rates that are quite a bit lower than in the North, around 10-20%. There are big gains to be made. However, there is considerably less construction going on now, for example in Spain or Italy, compared to 2005 - 2007. Cement plants in this region have lots of extra capacity and CO2 credits. There’s relatively little money or incentive for increased use of alternative fuels. The main response, which we’re starting to see now, is to close capacity in some of these countries. They are re-adjusting to a new reality.

More broadly, over all of Europe the European Commission is working to set substantially higher targets for paper and plastic recycling. This will have an effect on the amount of SRF feedstock. So too will the amount of landfill, which is set to fall massively in the future. In addition, supply to non-EU destinations will dramatically increase. These factors, plus a myriad of other considerations, will determine the future use of alternative fuels in Europe and beyond. It is not possible to forecast from this point how things will pan out. What I can say is that Cynosure is in a good position to make sense of situations as they unfold and to advise cement producers, municipalities and other parties on the best ways to maximise value for all stakeholders.

GC: It was great to speak with you today Andy. Thank you for your time.

AH: The pleasure is all mine!