This article looks at the cement sectors of the six Gulf Cooperation Council (GCC) nations to coincide with the 24th Arab-International Cement Conference & Exhibition, as well as an update about host nation Egypt.

The Cooperation Council for the Arab States of the Gulf, colloquially known as the Gulf Cooperation Council (GCC), is a regional political and economic union of six nations: Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, and the United Arab Emirates (UAE). Established in 1981, the GCC’s members are all Arab monarchies that have historically relied on oil revenues to fuel their economies. The two other Arab monarchies, Jordan and Morocco, are in discussions with the GCC regarding membership. Yemen had been due to join the GCC in 2015 but has not done so to date.

Over the past 38 years, the GCC has fostered links between the six member states on a number of levels. It has operated a shared military arm since 1984, a common market since 2008 and a customs union since 2015. Discussions towards monetary union, scheduled to be realised in 2010, took a knock in 2006 when Oman said it could not be ready in time. The project received another blow in 2009 when the UAE withdrew from the project after it was announced that the planned central bank for the new currency would be in Riyadh rather than in the UAE. Plans for a full single market were also delayed at around the same time, ostensibly due to the financial crisis. Over the longer term, the GCC’s other aims include GCC-wide approaches to tourism, legislation, scientific and technical research, agriculture, water resources, encouraging diversification away from the oil sector and ‘strengthening ties between its people.’

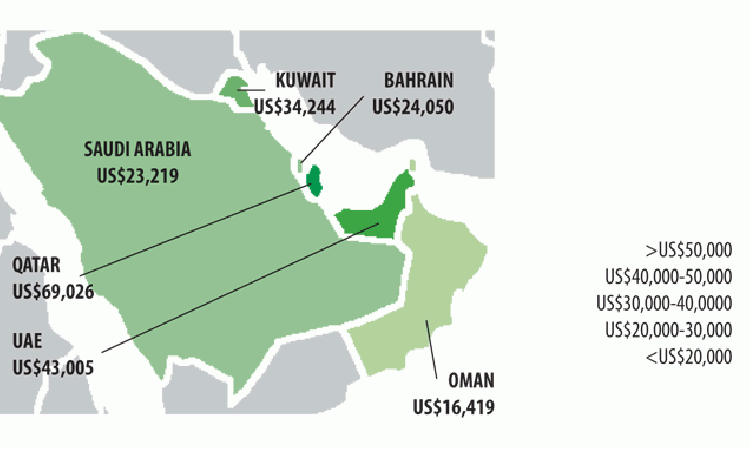

GCC cement by country

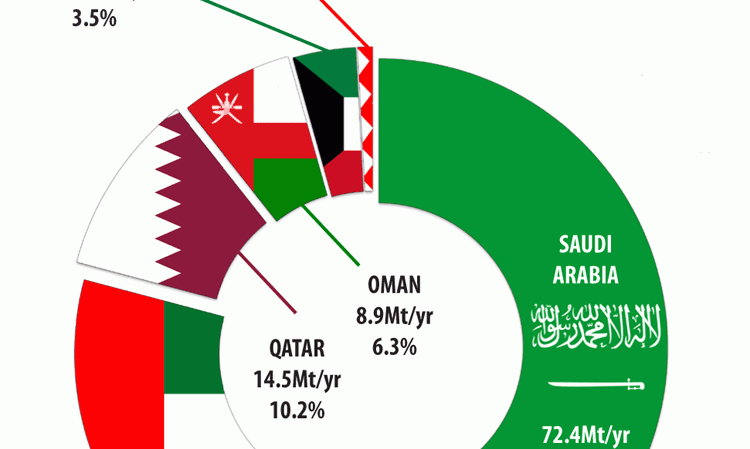

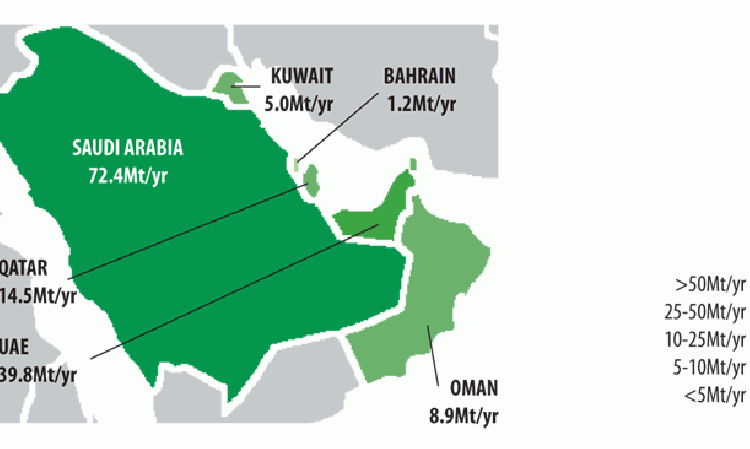

There are 40 active integrated cement plants in the GCC that share a total of 127.1Mt/yr of capacity. There are also 12 grinding plants that add a total of 14.7Mt/yr of capacity. This takes the GCC’s total to 141.8Mt/yr across 52 facilities. The Saudi cement sector is the largest in the GCC, with 72.4Mt/yr across 19 integrated and two grinding plants. This represents just over half (51.1%) of the GCC’s cement capacity. The second-largest cement industry in the GCC is that of the UAE, which has 13 integrated plants (30.1Mt/yr) and seven grinding plants (9.7Mt/yr), which combine to give it 39.8Mt/yr. The six national cement sectors are shown in Table 1 and Figure 1.

| Country | Integrated (Mt/yr) | Grinding (Mt/yr) | Total (Mt/yr) |

| Saudi Arabia | 70.4 | 2 | 72.4 |

| UAE | 30.1 | 9.7 | 39.8 |

| Qatar | 13.6 | 0.9 | 14.5 |

| Oman | 7.2 | 1.7 | 8.9 |

| Kuwait | 5 | 0 | 5 |

| Bahrain | 0.8 | 0.4 | 1.2 |

| TOTAL | 127.1 | 14.7 | 141.8 |

Above - Table 1: GCC countries, ranked according to installed cement capacity in 2019. Source: Research towards Global Cement Directory 2020.

GCC cement producers

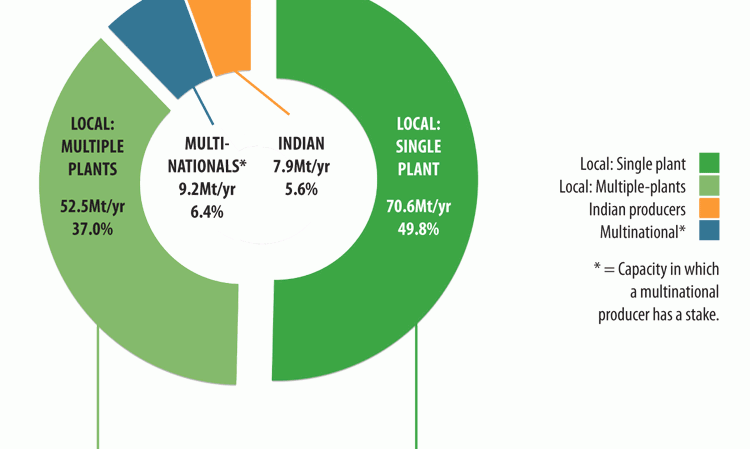

The GCC is unusual in that its cement sector is dominated by small local and regional players, often with just one cement plant. Figure 2 shows that producers with just one site operate 24 cement plants in the GCC, sharing a total capacity of 70.6Mt/yr, 51.9% of capacity. Locally-owned producers with multiple sites operate a further 52.5Mt/yr of capacity across 20 plants, giving local producers a total of 123.1Mt/yr, 86.8% of the GCC’s capacity. Indian producers operate four cement plants in the GCC, sharing 7.9Mt/yr (5.6%) of the region’s capacity.

The two global multinationals present in the region are LafargeHolcim and Cemex, which have stakes in plants with 9.2Mt/yr of capacity. Cemex operates 1.6Mt/yr of capacity outright via a single grinding plant, making it the smaller of the two. When LafargeHolcim’s minority stakes are taken into account, it operates 3.3Mt/yr of capacity via three different interests. Combined the two multinationals shares come to 4.9Mt/yr, around 3.4% of the GCC’s capacity. Local players hold the remaining shares in these plants.

| Rank | Company | Capacity (Mt/yr) | Headquarters |

| 1 | Southern Province | 15.7 | Saudi Arabia |

| 2 | Qatar National CC | 13.6 | Qatar |

| 3 | Saudi Cement | 6.4 | Saudi Arabia |

| 4 | Najran Cement | 6.3 | Saudi Arabia |

| 5 | Yanbu Cement | 5.7 | Saudi Arabia |

Above - Table 2: Top five cement producers in the GCC by installed capacity. Source: Research towards Global Cement Directory 2020.

Saudi Arabia

With 72.4Mt/yr of capacity, Saudi Arabia has by far the largest cement sector in the GCC. It almost entirely comprises Saudi-owned companies, the largest being Southern Province Cement (SPC), which has three plants and a total capacity of 15.7Mt/yr. SPC is also the largest individual producer by installed capacity in the GCC. Saudi cement producers are shown in Table 3.

| Producer | Plants | Capacity (Mt/yr) |

| Southern Province | 3 | 15.7 |

| Saudi Cement | 2 | 6.4 |

| Najran Cement | 2 | 6.3 |

| Yanbu Cement | 1 | 5.9 |

| Arabian Cement | 1 | 4.2 |

| Qassim Cement | 1 | 4.2 |

| Al Safwa Cement | 1 | 4 |

| Saudi White Cement | 1 | 3.7 |

| City Cement | 1 | 3.6 |

| Eastern Province | 1 | 3.5 |

| Al Jouf Cement | 1 | 3.5 |

| Tabuk Cement | 1 | 3.2 |

| Northern Region Cement | 1 | 2 |

| Umm Al Qura Cement | 1 | 2 |

| United Cement | 1 | 1.9 |

| Hail Cement | 1 | 1.6 |

| Al Gharibah Cement | 1 | 0.7 |

| TOTAL | 21 | 72.4 |

Above - Table 3: Saudi Arabian cement producers. Source: Research towards Global Cement Directory 2020.

Recent trends

Despite its high capacity, the Saudi cement market has suffered from overcapacity in recent years, making 45Mt in 2018 according to the USGS, a 4.4% decrease compared to 2017 when it made 47.1Mt. The 2018 utilisation factor was around 63%. The country had previously made as much as 61.9Mt in 2015. The reduction in cement production has been predominantly due to delays to major government infrastructure projects.

The combined net profit for 15 listed cement companies in Saudi Arabia was US$185m in 2018, around a tenth of value seen in 2014, according to Bloomberg. The situation has improved somewhat since the relaxation of export regulations in July 2017, with 25Mt exported in the two years to July 2019. Previously scarce, Saudi-made cement can now be found all around the GCC, as well as further afield. Abdul Rahman Hussein, from the Ministry of Trade and Investment, noted that 53 cement export licences were issued between July 2017 and July 2019, with 22 issued since the start of 2019. At the same time he warned that, following a two year tax holiday, the government was now looking to charge exporters for taking cement out of the country.

Finances in 2019

In the first half of 2019, the major Saudi cement producers have reported improved fortunes. SPC’s sales revenue rose by 37% year-on-year to US$165m in the first half of 2019 from US$121m in the same period in 2018. Its net profit after Zakat and tax grew by 53% to US$56.3m from US$36.8m. Number two producer Saudi Cement’s sales revenue rose by 26% to US$194m in the same period, with its net profit after Zakat and tax rising by 12% to US$59.9m. Third-placed Najran Cement’s sales also improved by 20%, to US$48.7m, with a profit after Zakat and tax of US$920,000. Najran separately announced that it would increase production by restarting one of its three kilns in June 2019. While not explicitly stated by these producers, it is likely that increased exports have helped many cement producers in Saudi Arabia.

Recent news

Denmark’s FLSmidth revealed that it is working on a project to convert a grey cement production line at Al Safwa Cement to a dual white and grey line in June 2019. The modified kiln is expected to be commissioned in early 2020. The production objectives are to produce a minimum of 2000t/day white clinker with a maximum heat consumption of 1380kCal/kg clinker. No value for the project has been disclosed. A white kiln conversion is also being carried out at Al Jouf Cement, which signed a non-binding memorandum of understanding with China’s Riga Company in April 2019.

Yamama Cement is also upgrading its production facilities, by selling its five old kilns as part of a move to a new site. The five kilns were ‘temporarily’ shut in 2017 due to economic conditions, but remained uneconomic in the longer term, prompting Yamama to offer them for sale in October 2019. The company is in the process of building a new 6.4Mt/yr plant near Riyadh with two dry lines from thyssenkrupp Industrial Solutions.

UAE

The UAE has a diverse cement sector (Table 4), with Omani, Indian and local players, as well as LafargeHolcim and Cemex. Like its larger neighbour Saudi Arabia, the UAE has struggled with cement overcapacity recently as its rampant construction finally slows down. The UAE only consumes half the cement that it can make, around 21Mt in 2018. Cement is exported to other GCC countries, as well as to Africa.

| Producer | Plants | Capacity (Mt/yr) |

| Arkan Cement | 1 | 5.7 |

| Union Cement (Shree Cement) | 1 | 4.8 |

| Star Cement (Aditya Birla) | 1 | 4.5 |

| Gulf Cement | 1 | 3.6 |

| National Cement (44% LH) | 2 | 3.5 |

| Lafarge Emirates (50% LH) | 1 | 3.2 |

| Fujairah Cement | 1 | 2.4 |

| Binani Cement (UltraTech) | 1 | 2 |

| Sharjah Cement | 1 | 2 |

| Pioneer Cement (Raysut Cement) | 1 | 1.7 |

| Cemex | 1 | 1.6 |

| Teba Cement | 1 | 1.2 |

| JK White Cement | 1 | 1 |

| RAK Cement | 1 | 1 |

| Jebel Ali Cenent | 1 | 0.8 |

| RAK White Cement | 1 | 0.8 |

| TOTAL | 17 | 39.8 |

Above - Table 4: Cement producers in the UAE. LH = LafargeHolcim. Source: Research towards Global Cement Directory 2020.

Finances in 2019

Arkan Cement’s profit grew in the first half of 2019 due to the sale of a previously closed 1.0Mt/yr integrated plant in February 2019. Arkan also benefited from cost controls and an insurance claim. Its profit more than doubled to US$12.4m in the first half of 2019 from US$4.67m in the same period in 2018. However, its sales revenue fell by 9.6% to US$79m from US$85.2m. It blamed ‘price pressure’ due to a declining export market. RAK Cement’s sales fell by 20% year-on-year to US$254m in the first half of 2019, compared to US$31.7m in the first half of 2018. Its profit fell by 79% over the same period to US$29.1m.

Recent news

The overcapacity in the UAE cement market appears not to have deterred Fujairah Natural Resources, which announced in February 2019 that it would invest in a new US$150m integrated plant in Habbab, Fujairah. However, a financing failure put a stop to RAK Cement’s intended US$123m purchase of the JK White Cement plant and its associated quarry, also in Fujairah, in September 2019.

To better navigate this oversupplied market, Arkan subsidiary Al Ain Cement and National Cement signed a clinker offtake deal in July 2019. Al Ain Cement will supply clinker from its plant in Al Ain to National Cement’s Abu Dhabi grinding plant.

Finally, UltraTech Cement has been trying to offload Star Cement since May 2019. It has not yet found a buyer. The Star Cement assets came as part of the larger Binani Cement acquisition between the two Indian enterprises in 2018.

Qatar

The cement sector of Qatar is dominated by Qatar National Cement Company (QNCC), which operates four distinct integrated plants, all at Umm Bäb. These share a combined 8.6Mt/yr of cement capacity, with sizes ranging from 0.6Mt/yr to 5.0Mt/yr. QNCC has operated in Qatar since 1965, when it opened its first plant. The company opened its second plant in 1998 (0.6Mt/yr) (having previously extended the first) and opened the third (1.4Mt/yr) in 2007. Plant four (5.0Mt/yr) came online in 2009 and plant five (1.6Mt/yr) began operations in late 2018. Plant one, which had a capacity of 0.3Mt/yr, has since been closed. QNCC made its first white cement in December 2018. In April 2019 it announced that it was preparing to export up to 3Mt/yr of cement from its combined operations. Quite where this will all be used is an open question, given the overcapacity affecting the wider GCC region.

The second-largest cement producer in Qatar is Al Khalij Cement, part of Qatari Investors Group, which operates a 5.0Mt/yr integrated plant, also in Umm Bäb. It commissioned its first 2.5Mt/yr FLSmidth line in 2007 and added a second in 2015. The third and final player in the Qatari cement industry is Al Jabor Cement Industries, which operates a 0.9Mt/yr grinding plant in Doha. It is 25% owned by LafargeHolcim.

Recent finances and news

QNCC recorded sales of US$2.2bn in 2019, with a net profit of US$903.5m. The revenue figure was 18% down year-on-year compared to 2017, when the company saw sales of US$2.69bn. However, the profit made in 2018 was actually 6.4% higher than the US$849.2m profit recorded in 2018.

In March 2019, Al Khalij signed a three year deal to supply oil well cement to Qatar Petroleum. The agreement was signed by Qatar Petroleum’s Executive Vice President Mohamed Al Marri and Qatari Investors Group CEO Raja Assili. The plant obtained its API Monogram in November 2018.

Kuwait

There is one integrated cement plant in Kuwait, operated by Kuwait Cement Company. The 5.0Mt/yr plant is located in Shuaiba and started out as a 0.3Mt/yr grinding plant in 1972. It underwent various upgrades over the years before gaining its own kiln in 2009.

ACICO is in the process of building a 1.0Mt/yr grinding plant in Kuwait. A 5200 Kws ball mill with all the peripheral equipment from Cemengal and a fourth generation XP4i-130 classifier from Magotteaux were contracted in February 2019 to complement a prior order. The plant is expected to be commissioned in the first half of 2020. It may face a tough market given that Saudi and Iranian cement producers are increasingly targeting the Kuwaiti market. Saudi-based Qassim Cement made its first exports to Kuwait in March 2019.

Recent finances and news

Kuwait Cement’s profit fell by 19% year-on-year to US$10.2m during the second quarter of 2019 and fell by a third in the first half of the year to US$14.9m. The company noted that the decline in first half profit was attributed primarily to lower income from its investments, as well as to a drop in cement revenues.

Meanwhile, Kuwait Cement hired Belgium’s Magotteaux to modernise three of its cement mills in March 2019. The project consisted of closing the open circuit with fourth generation XP4i separators, installing new mill internal components, including diaphragms, and adapting a new ball charge gradation. The aim of the project was to increase production, while reducing specific energy consumption and improving product quality.

Oman

There are three active cement plants in Oman, giving it a capacity of 8.9Mt/yr. The largest producer is Raysut Cement (4.7Mt/yr), which operates one integrated plant (3.0Mt/yr) and one grinding plant (1.7Mt/yr). It acquired the grinding plant, formerly Sohar Cement, in May 2019. Oman Cement operates the largest individual plant, a 4.2Mt/yr integrated facility in Muscat.

Recent finances and news

There will be a fourth cement plant in Oman in the near future, following an agreement between the Port of Duqm and Raysut Cement in late September 2019. The latter will build a US$30m, 1.0Mt/yr grinding plant having earlier received a US$50.7m grant from Bank Nizwa to support economic diversification in the Sultanate. In the longer term, Raysut is looking to build a 1.8Mt/yr integrated plant, also at Duqm. This larger investment is expected to cost in the region of US$210m. Raysut appointed a consultant to the project on 12 September 2019.

Aside from its investments at home, Raysut Cement is one of the most geographically diverse cement producers in the GCC. It operates capacity in the UAE, East Africa and the Caucasus, with its sights set on the Indian market in the medium term.

Despite these lofty investment aims, Raysut Cement actually saw a deterioration in its ongoing operations in the first half of 2019. Its revenue fell by 5% year-on-year over the six month period to US$108m from US$114m in the first half of 2018.

Oman Cement reported revenues of US$132m in 2018, a 12% fall year-on-year compared to US$150m in 2017. Its profit also fell by 24% to US$19.0m in 2018 from US$24.9m in 2017.

Bahrain

The smallest cement producer in the GCC, Bahrain, has two cement plants (1.2Mt/yr), the 0.8Mt/yr integrated Falcon Cement plant in Hafirah and the 0.4Mt/yr Star Cement (UltraTech Cement) grinding plant in Manama. Falcon began operation in March 2009 with a capacity of 0.3Mt/yr but has expanded to 0.8Mt/yr in 2015. Its website states that it will expand to a capacity as large as 1.1Mt/yr during 2019 but there is limited detail regarding progress towards this target.

Egypt

Egypt is predominantly located in Africa, although around 6% of its land area, the Sinai Peninsula is within Asia. It is not part of the GCC, but is culturally aligned in many ways. Indeed, representatives from Bahrain called for Egypt to join the GCC in 2011 but this has not since transpired.

Egypt has a larger cement sector than any country in the GCC, marginally beating Saudi Arabia by 78.3Mt/yr to 72.4Mt/yr. The majority of its capacity was added in the 1970s and 1980s, before the regime of Hosni Mubarak privatised the sector in the 1990s. This time saw an influx of foreign investment, including from the multinationals shown in Table 5. Today Egypt has 23 integrated plants (74.6Mt/yr) and three grinding plants (3.7Mt/yr).

Cement sector - Producers

| Producer | Plants | Capacity (Mt/yr) |

| El-Arish Cement | 1 | 13 |

| HeidelbergCement | 5 | 11.9 |

| Lafarge Cement Egypt (LH) | 1 | 10.6 |

| Assiut Cement (Cemex) | 1 | 5.7 |

| Amreyah Cement (InterCement) | 1 | 5.5 |

| Arabian Cement | 1 | 5 |

| Misr Beni Suef Cement | 1 | 3.5 |

| Misr Qena Cement (27% ASEC) | 2 | 3.4 |

| Beni Suef Cement (Titan) | 1 | 3.2 |

| South Valley Cement | 2 | 3.1 |

| Alexandria Portland (Titan) | 1 | 2 |

| Wadi El Nile Cement | 1 | 2 |

| Sinai Cement (41% Vicat) | 1 | 1.9 |

| El Nahda Cement | 1 | 1.7 |

| BMIC | 1 | 1.5 |

| El Sewedy Cement | 1 | 1.5 |

| Sinai White (57% Cementir) | 1 | 1.2 |

| Medcom Cement | 1 | 0.8 |

| SPEGYCO | 1 | 0.6 |

| Royal El Minya Cement | 1 | 0.2 |

| TOTAL | 26 | 78.3 |

Above - Table 5: Cement producers in Egypt. LH = LafargeHolcim. Source: Research towards Global Cement Directory 2020.

The story of Egypt’s largest cement producers is partly a tale of the country’s largest plants. The largest producer is El-Arish Cement, which has a single plant in Beni Suef. Opened in April 2018, the plant has a capacity of 13.0Mt/yr across six identical dry process lines. This plant alone represents around 17% of national capacity.

The second-largest producer is HeidelbergCement, which operates five integrated plants through its subsidiaries Suez Cement (2 plants, 5.4Mt/yr), Helwan Cement (2 plants, 5.5Mt/yr) and Tourah Portland Cement (1 plant, 1.0Mt/yr). Its 11.9Mt/yr capacity provides it with 15% of national capacity.

The third-largest producer is LafargeHolcim, which, like El-Arish Cement, only operates one plant. However, the plant has a capacity of 10.6Mt/yr, sufficient to provide it with 14% of Egyptian capacity.

Recent trends

Egypt’s cement sector has been battered by several logistical and economic issues in recent years, in addition to prolonged political uncertainty. Demand took a hit after the Arab Spring and domestic consumption remains far below capacity. This has lowered the price producers can realise in the market.

At the same time fuel shortages, which began in 2013 due to a reduction in government fuel subsidies to heavy industries, have eaten into producer margins from the other direction. The price of mazut, a form of heavy fuel oil, increased by a factor of 2.5 over the six months from January to June 2013. Over the past five years this has prompted a wide-spread switch to coal imports and alternative fuels. While less costly than mazut, Egyptian cement producers are now paying significantly more for fuels than before this change in government policy.

Then, just as a ‘new normal’ had been established, the government increased energy prices in June 2018, piling further pressure on margins. Cement exports, the refuge of several producers, became uncompetitive. Then, the government-backed 13.0Mt/yr El Arish Cement plant came online in April 2018. It was not well received by other produers and has exacerbated the mismatch between supply and demand. Smaller producers have been feeling the heat in particular, as expanded upon below. However, more recently the government reduced the price of natural gas for cement producers to US$5 per one million British thermal units (BTU). Previously the price was US$8. It will now review the price of gas every six months.

Cement sales in Egypt fell by 7.7% year-on-year to 10.9Mt in the first quarter of 2019. Data from the Central Bank of Egypt shows that production fell by 8.1% to 11.2Mt. In August 2019, Medhat Istafanos, the head of the Cement Division at the Federation of Egyptian Industries (FEI), stated that domestic cement demand was supporting only 40% of local production. He blamed this on a slowdown in building activity and a lack of government-backed infrastructure projects. He reported that only 48Mt of cement was sold in 2018.

Producers are exploring options to increase cement exports. Walid Gamaleddin, the president of the Export Council for Building Materials and the Metallurgical Industries, has called for the government to support industry exports. The minister of trade and industry discussed a programme for cement-export subsidies with officials from the sector in late July 2019 that would include encouraging agreements to export cement to the African countries. The Central Bank of Egypt (CBE) has also instructed the banking sector to support cement companies that need to restructure their debts. The merger of smaller companies to form larger conglomerates has also been encouraged.

However, growing exports of Egyptian cement is challenged by its relative high cost compared to other countries. Istafanos said that Egyptian cement is US$12/t higher than its competitors.

Recent finances and news

The relentless squeezing of margins in Egypt’s cement sector has affected many producers so far in 2019. Misr Beni Suef Cement reported net profits for the six months to 30 June 2019 of US$2.76m, a massive 78.8% lower than the US$13.0m that it made during the same period of 2018. This is part of a wider profit slump for Egyptian domestic cement producers, with Misr Cement Qena’s first half figure down by 85.2% to US$0.87m from US$6.00m a year ago. Elsewhere, South Valley Cement reported losses of US$6.19m in the first half of 2019, compared to a US$1.27m profit in the same period of 2018. Meanwhile, Sinai Cement recorded a first half net loss of US$11.3m, an increase of 20.1% on the loss recorded in the same period of 2018. Suez Cement made a loss during the first half of 2019. Its net loss reached US$17.7m over the six month period, from a profit of US$14.4m in the first six months of 2018. The company generated US$199m in revenue during the first six months of 2019, compared to US$238m a year earlier.

In September 2019 Alexandria Portland Cement, one of HeidelbergCement’s subsidiaries, was forced to sell land to stave off losses. It sold a 15.9km2 parcel of disused land in Ad Dakhila for US$1.9m. The company made a loss of US$10.3m in the first half of 2019. Some went even further, with El Nahda Cement taking the drastic step of suspending production at its 1.7Mt/yr plant at Quena for six months in July 2019.