The Republic of the Philippines is a large archipelagic nation in South East Asia. Unusually for the region, the country is predominantly Christian, a characteristic it traces back to its 377 years as a Spanish colony and 44 years as a US protectorate. Fully independent since 1946, the country is today classified as ‘newly industrialised,’ with the sixth-largest economy in Asia, with a GDP of US$877bn in 2017. Its economy was relatively resilient to the economic shocks of the 2010s, with strong domestic consumption and low unemployment.

However, the country’s wealth has been spread unevenly, both within major cities and between cities and poorer rural communities. This was one of a number of contributing factors to the election of the current nationalist President Rodrigo Duterte in June 2016, ostensibly on a poverty alleviation ticket. As well as running a notorious campaign against criminal gangs, which Duterte claims represent a major barrier to wealth generation and distribution, the nation’s poor infrastructure was also identified as an obstruction to growth. In 2017 the administration pledged that US$165bn would be spent on infrastructure by the end of Duterte’s term in 2022. The government’s ‘Build Build Build’ programme is driving construction across the country. Major projects include a proposed new US$14bn airport for the capital Manila and a plethora of highways, railways, water projects and public buildings.

Cement demand, production and prices

The strong emphasis on construction has been fantastic news for the country’s cement producers. Cement sales rose from 24.4Mt in 2015 to 26.0Mt in 2016, according to the Cement Manufacturers Association of the Philippines (CMAP). While CMAP no longer publishes cement sales figures for the sector, other sources indicated at the start of 2019 that demand had reached 32Mt/yr, with domestic suppliers only able to provide 27Mt/yr. The Department for Trade and Industry reports that the balance has been made up by imports, which increased from just 3558t in 2013 to 3Mt in 2017 and then 5Mt in 2018.

Following a period during which it was free to import cement into the Philippines, a US$4/t import duty was implemented in January 2019. This did not appear to have a significant impact on cement imports during the first quarter of 2019. Indeed, imports rose by 64% during that period to 1.74Mt, according to the Philippine News Agency.

On September 2019 the DTI introduced a permanent customs duty on imported cement of US$4.81/t. The Manila Times reports that the measure is subject to annual review and will be in place for three years, decreasing by US$0.48/t/yr. Philippine law allows for the imposition of such measures where an appointed advisory body has determined that increased imports ‘threaten to substantially cause injury to the domestic industry.’ The advisory body in question is the Tariff Commission, which had previously suggested a levy as high as US$5.68/t.

Trade Secretary Ramon M Lopez said that the government needed to take care to manage imports while allowing the construction sector to continue to grow. The impact on cement prices has been moderate. From US$98.6/t in early January 2019, they reached US$108.25/t by September 2019. Vietnamese producers have been the largest beneficiaries of the price hike, with 75% of the Philippines’ imported cement originating in Vietnam.

When the levy was announced, the Philippine Competition Commission (PCC) said that it would impact upon its investigations into an alleged ‘cartel’ of cement producers dating from 2017. PCC Chair Arsenio Balisacan noted that it was a clear danger to have ‘an ongoing investigation and introducing a policy that could influence the outcome of that investigation.’

Elsewhere, there have been rumours since at least February 2019 that the DTI would introduce a maximum price on cement in order to protect local construction firms from high prices. However, this has not been deemed necessary so far.

Cement plants on the ground

There are 16 active integrated cement plants in the Philippines that share a combined capacity of 33.6Mt/yr, according to research undertaken towards the publication of the Global Cement Directory 2020. The country is also home to three active grinding plants with a total of 2.2Mt/yr. Taken together, these 19 plants have a headline capacity of 35.8Mt/yr of cement. There are also two closed / mothballed integrated plants and two under construction, as well as three mooted grinding plants.

Figures 1 & 2 show that the majority of cement production capacity in the Philippines is located in the most populous areas. This is clearest in the region surrounding the capital Manila. The three most populous regions, Calabarzon, the National Capital Region (NCR) and Central Luzon, are home to 38.6 million of the Philippines’ 105 million inhabitants, 37% of the population. However, their combined cement capacities are 20.4Mt/yr, 57% of capacity.

Cement producers background

The past five years have been a time of significant change for the cement sector in the Philippines. Prior to the announcement of the LafargeHolcim merger, the two dominant players were Holcim Philippines (85.5% Holcim) with 7.6Mt/yr of capacity, and Lafarge Republic (100% Lafarge), which operated 5.6Mt/yr of capacity. In July 2014 it was proposed that Lafarge Republic and Holcim Philippines would explore the combination of their businesses other than Lafarge’s Bulacan, Norzagaray and Iligan plants, which would have to be divested.

These were sold to Ireland’s CRH, which took on the assets of Lafarge Republic Inc., Luzon Continental Land Corporation and Lafarge Cement Services Philippines, Inc., including assets related to the Bulacan quarry. LafargeHolcim kept Lafarge Iligan, Inc., Lafarge Republic Aggregates, Inc., Lafarge Mindanao, Inc., and certain assets related to the STAR Terminal and the Pinagtulayan islands. On 18 May 2015 it was announced that Aboitiz Equity Ventures Inc had signed a deal to join CRH as a joint-venture partner.

Top 5 players in 2020

LafargeHolcim: The largest cement producer in the Philippines at the start of 2020 is the Swiss-French giant LafargeHolcim, which operates 9.9Mt/yr of capacity across four integrated plants (9.1Mt/yr) and one grinding plant (0.8Mt/yr).

LafargeHolcim added 0.7Mt/yr of capacity to its Davao plant in 2019. The expansion involved the commissioning of a finish mill and installation of a new pipe for loading cement to the plant’s silos from its pier, eco-hoppers to improve dust emissions and an overhead crane. Cold commissioning started in April 2019, while full production began in late June 2019. The company is also upgrading its 3.3Mt/yr Bulacan plant to 5.3Mt/yr, to give a future capacity of 11.9Mt/yr.

Holcim Philippines improved its profit in the third quarter of 2019 by 158% year-on year to US$9.00m from US$3.48m. Its sales in the quarter fell by 2.7% year-on-year to US$163m from US$167m in 2018. The company sustained price increases in spite of lower demand causing a fall in volumes. Holcim Philippines’ sales in the first nine months of 2019 fell by 13% to US$465m from US$536m in the corresponding period to 30 September 2018. Upgrades to its La Union and Davao cement plants in previous quarters dragged on nine-month profit, which rose by 7.9% year-on-year to US$36.9m from US$34.2m in the corresponding period of 2018, but paid dividends in the third quarter, boosted by the resumption of state infrastructure spending.

Eagle Cement: Eagle Cement (7.7Mt/yr) is the second-largest cement producer in the Philippines. It is locally-owned and has been making cement since 2010. In 2020 it operates a three line 7.1Mt/yr integrated plant and 0.6Mt/yr grinding plant.

At the start of 2019 Eagle Cement’s integrated plant was already the country’s largest, with two kiln lines and 5.1Mt/yr of capacity. In 2019 a third line was added, providing an additional 2.0Mt/yr of capacity. The producer will shortly add a further 1.5Mt/yr of clinker grinding capacity to the plant to fully unleash its integrated plant’s capabilities and take its overall capacity to 8.4Mt/yr. It is also building a 2.0Mt/yr plant in Cebu.

Eagle Cement continued its positive earnings momentum in the first nine months of 2019, with a 35% year-on-year increase in net income to US$91.9m. Its sales for the period were US$299m, a year-on-year rise of 19%.

CRH-Aboitiz: The third largest producer and second multinational by installed capacity in the Philippines is CRH-Aboitiz, via the subsidiary Republic Cement (6.9Mt/yr). Republic Cement is the third largest operator overall. It runs five integrated cement plants (6.1Mt/yr) and one grinding plant (0.8Mt/yr).

CRH’s global sales revenue grew by 4% on a like-for-like basis to Euro21.8bn in the first nine months of 2019. Its earnings before interest, taxation, depreciation and amortisation (EBITDA) rose by 7% to Euro3.2bn. The group reported lower sales in the Philippines, which it attributed to a general slowdown in infrastructure spending over the nine month period as a whole.

Cemex: The Filipino subsidiary of Mexican cement major Cemex is the fourth-largest cement producer in the country and third-largest multinational via two subsidiaries: APO Cement and Solid Cement. It entered the market in 1997 and today operates two integrated plants (6.2Mt/yr).

Cemex Philippines ordered an MVR type mill for cement raw material grinding from Germany’s Gebr. Pfeiffer for its Solid Cement plant in Antipolo in October 2019. The order also included an MPS mill to grind coal. The order was received through a Chinese general contractor but no value or timescale was disclosed.

Cemex Philippines recorded a profit of US$17.1m in the nine months to 30 September 2019, compared to a loss of US$13.0m in the corresponding period of 2018. The company attributed the turn-around to steadily growing sales, up by 1.7% year-on-year to US$360m from US$350m, foreign exchange gains and lower income tax expenses, in spite of falling domestic volumes.

Taiheiyo Cement: The Japanese cement producer Taiheiyo Cement operates a 2.3Mt/yr integrated cement plant in Cebu, which is currently undergoing expansion to 5.2Mt/yr.

Smaller players

The top five cement producers in the Philippines share 33.0Mt/yr (92%) of the country’s capacity. A further three share the remaining 2.8Mt/yr (8%) of capacity across three integrated plants.

Northern Cement Corporation (NCC) was established in 1967. NCC’s integrated plant in Pangasinan was upgraded extensively in the 1990s to a capacity of 1.2Mt/yr. NCC is reported to be in the process of building a second plant, a 2.0Mt/yr facility in Bulacan. The company is 35% owned by First Stronghold Cement.

Elsewhere, Goodfound Cement operates a 1.0Mt/yr integrated cement plant in Camalig, Albay, while Mabuhay Filcement operates a 0.6Mt/yr integrated plant in South Pobacion, Cebu.

Deals to watch in 2020

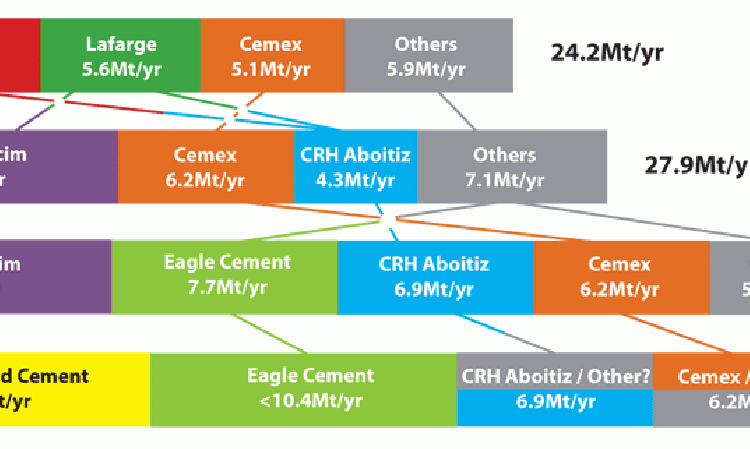

Those who followed the cement news in 2019 will know that the LafargeHolcim merger was only the start of major restructuring of the Philippines’ cement sector. This is because LafargeHolcim decided to exit the market in May 2019, when it agreed to sell its entire holding in the Philippines to San Miguel Corporation’s subsidiary First Stronghold Cement.

The multinational left the entire South East Asian market in a major readjustment of its global footprint in 2019. The company sold a total of 34Mt/yr of cement capacity as it left the region, cutting its capacity by around 12% to 278Mt/yr.

However, the deal with San Miguel has attracted the attention of the Philippine Competition Commission (PCC), which reported in November 2019 that it was considering voluntary commitments submitted by First Stronghold Cement and related parties. This is due to First Stronghold Cement already having a 35% stake in Eagle Cement, the country’s second-largest cement producer.

Initial findings by the PCC on the proposed purchase found it could affect the market concentration of relevant products in parts of Luzon, and Northern and Southern Mindanao. This would normally prompt a stage two review of the proposed acquisition. It is possible that divestments prior to completion of the deal could help avoid this step.

The transfer of Holcim Philippines to San Miguel Group, which is likely to be completed in 2020, will drastically alter the Philippines’ cement sector landscape (See Figure 3). This is before one even considers the potential sale of CRH-Aboitiz’s assets. CRH engaged JP Morgan to investigate the sale of its entire operation in the Philippines in November 2019. At the time, The Irish Times reported the estimated value of the divestment as Euro1.82-2.73bn. No buyer has come forward to date.

New plants on the horizon

With such significant imports heading into the Philippines in 2019, there is strong impetus to build new cement capacity in the country itself. Indeed, there are three major projects currently in the pipeline from a mixture of established producers and newcomers.

In June 2019 Eagle Cement announced that the opening of its new Malabuyoc integrated 2.0Mt/yr plant in Cebu has been delayed by six months to mid-2021. The new unit had been scheduled to start operation in late 2020 but has been delayed due to issues obtaining permits. The project will bring Eagle’s capacity to 10.4Mt/yr, perhaps enough to make it the market leader, depending on divestments elsewhere.

Big Boss Cement and Petra Cement are spending US$193m on cement grinding plant projects in Pampanga and Zamboanga. Big Boss Cement is building four cement lines at its Pampanga plant, while Petra Cement is building two lines at Zamboanga del Norte. Both companies have the same shareholders, led by prominent businessman Henry Sy Jr.

Company President Gilbert S Cruz said that the companies will spend US$135m at Pampanga plant and US$58m at the Zamboanga plant. Each line will have a cement production capacity of around 0.5Mt/yr. The company reports that construction of two production lines was completed at the Pampanga plant at the end of 2019 and that the remaining two are scheduled for completion in the first quarter of 2020. Big Boss Cement and its related companies also plan to build new plants at General Santos, Negros and Iloilo. It aims to reach a production capacity of over 5Mt/yr by the mid-2020s.

The company says it is using a ground activated sand by heating (G-ASH) process to produce a binding material for concrete that does not use imported clinker. It has claimed that it is the first cement company in the world to do so.

In October 2019 Phinma Corporation announced that it would spend US$50m on a new grinding plant at Bataan with a production capacity of 2Mt/yr. Philcement, a subsidiary of Phinma Corp. and Seasia Nectar Port Services (SNPS), have signed a deal to take over certain construction-in-progress assets, including the usage rights to pier facilities and land currently under lease by Philcement, for a terminal for US$15.5m, according to the Philippine Daily Inquirer newspaper. President and CEO Eduardo Sahagun said that the company would need up to US$35m to complete the project. Once competed it will be possible to expand the unit to 4.0Mt/yr, depending on market demand.

In addition to the above, the major Filipino construction conglomerate DCMI Holdings has hinted at a number of cement plant projects over the years, most recently in 2017, when it stirred rumours of a new integrated plant on Semirara Island in Western Visayas. It previously announced three grinding plants in 2016. However, none of these projects appears to have made it to completion at the time of publication.

Future

Figure 3 shows that, should all of the planned capacity additions be realised, the next two years to the end of 2021 could see the addition of a further 7.7Mt/yr of cement production capacity to 43.5Mt/yr. This is around 21% more than 35.8Mt/yr at present. While some projects may fall by the wayside, it seems very likely that the Philippines’ cement capacity will exceed 40Mt/yr in the near future.

There are still two and a half years of President Duterte’s six year Presidential term left. If the emphasis on ‘Build Build Build’-ing remains strong, the cement sector of the Philippines will be well supported by growing local demand as it expands its capacity.