Cement sector consultant Joe Harder introduces the key findings of OneStone Consulting’s new report Covid-19 Impact Analysis CIC 2025, which looks at how the outbreak will alter our sector in the period to 2025.

Global Cement (GC): Please could you introduce the report in a few sentences?

Joe Harder (JH): The CIC 2025 report is a new market report that provides clients with the latest market information about the impact of the on-going coronavirus pandemic on global cement production, with forecasts for 2020, 2021 and 2025. It draws on data taken from 75 countries that jointly represented almost 97% of all global cement capacity in 2019. There are forecasts for the world as a whole, 10 regional areas, four sub-regions in Europe and for the individual countries themselves. It is in executive style, with 109 pages, 70 figures and nine tables, available at a competitive price.

GC: Which audiences is it intended for?

JH: Our idea is to provide our customers in the cement industry with a master study on the impact of Covid-19, with three-month updates if necessary. The new report is intended for cement producers that want to analyse future demand trends, suppliers of equipment, analysts, traders and anyone else with an interest in the global cement industry.

GC: At what point in the outbreak did you decide to produce this the report?

JH: We had already decided to write the report at the start of February 2020, as we had to update a five-year strategic planning report for one of our clients in the cement equipment manufacturing sector.

GC: What data does the report draw upon?

JH: The report relies on data from a number of well-respected sources. We have used the IMF’s April 2020 World Economic Outlook (WEO), which looks at GDP growth, as a measure of the likely damage caused by Covid-19 to various economies around the world. GDP is a crucial factor in assessing future construction spending and cement demand. We also took into consideration the longer-term forecasts from the October 2019 WEO.

We have also considered historical cement production data for 2005 - 2017, as this provides a baseline to what growth we might expect under ‘normal’ conditions. This information was obtained from numerous sources, including national and regional associations and cement producers themselves. More attention was paid to changes in 2018 and 2019, with monthly figures used for these years, plus data for the first quarter of 2020, where available. We have also considered changes to operations due to various coronavirus-related lockdowns around the world.

As part of this, we have looked at projections as to how the coronavirus pandemic will develop in various countries to estimate how long different construction sectors will be affected. With below 5 million cases at present, it is clear that the world needs time to achieve ‘herd immunity’ to this virus. What we see at present for a large number of countries is that the peak of the virus probably, hopefully, passed around the end of April 2020 to mid-May 2020. The IMF presumes that there is a general reduction in cases in the second half of 2020, with fairly significant resumption of economic activity in most markets by the start of 2021.

GC: What does the IMF say about growth in the coming 12 months?

JH: The IMF has revised its projections dramatically in its April 2020 WEO. Global GDP is now expected to fall by 3.0% in 2020, following a 2.9% rise in 2019. For 2021, however, it expects a major reversal of economic fortunes around the world, with global GDP growth of 5.8%. If realised this will make up for the losses seen in 2020.

The depth of the trough will not be consistent around the world, however. Developed economies are currently forecast to lose out the most in terms of GDP in 2020, with a contraction of 6.1% year-on-year. Meanwhile, developing economies are forecast to shrink by only 1.0%. In 2021 the ‘bounce-back’ will be 6.6% in developing economies according to current projections, with a lower 4.5% growth forecast for developed economies.

Of the developed markets, the EU is expected to fare worst, with a 7.5% decline in economic output in 2020. The US is expected to suffer a 5.9% contraction, with South America also performing fairly badly. The Middle East and Africa, which have not, so far, suffered quite the massive outbreaks that Asia, Europe and North America have, will contract in the 2 - 3% range in 2020. I am personally surprised that the GDP decline in 2020 is expected to be only 3.0%. However, most surprising is that the IMF expects both India and China to grow their economies in 2020, by 1.9% and 1.2% respectively.

GC: How will cement production be affected by the outbreak?

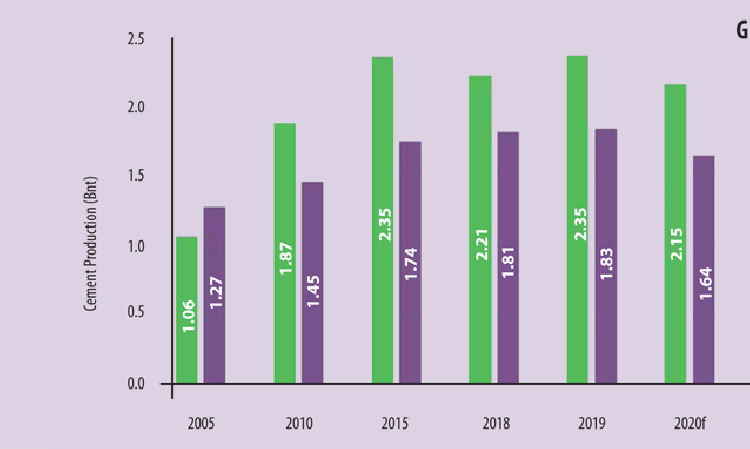

JH: Our projections show that producers should expect a year-on-year decline in global cement production of 9.3% in 2020 compared to 2019. For China, the decrease is projected to be 8.5% and for the rest of the World it is forecast to be 10.4%. For 2021, we forecast a recovery of 8.0% across the rest of the World but a 3.3% fall in production in China. This works out at an overall rise of 1.6% compared to 2020.

The change in China, by this point, will not be due to coronavirus-related effects, but rather a continuation of China’s supply side demand changes. Before the coronavirus we already expected production to fall by about 2% in 2021 compared to 2020. This needs to be considered when looking at these figures.

GC: Can you break down the regional findings in more detail?

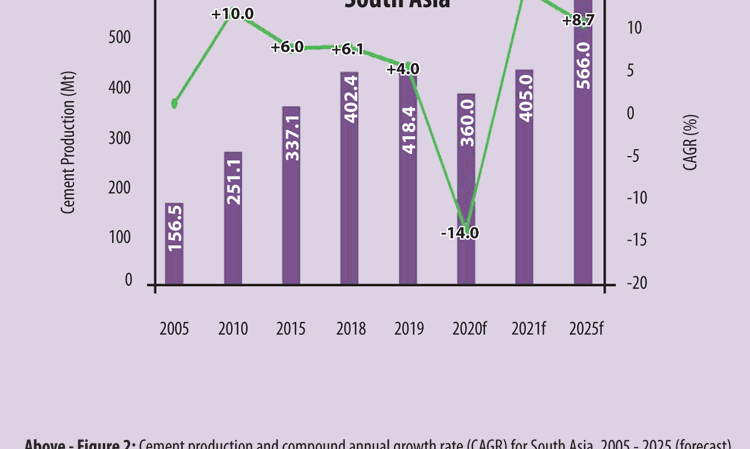

JH: The most dramatically affected region, by our projections, will be South Asia, comprising India, Pakistan, Bangladesh, Sri Lanka, Bhutan, Nepal and Afghanistan. This will see a 14.0% reduction in cement production in 2020 compared to 2019, but then a massive rebound by 12.5% in 2021 compared to 2020. Unlike some other regions, it will not have a chance to recover in the third quarter of 2020 due to the monsoon season, which sees an annual reduction in construction activities. This will hit producers hard, especially as India in particular had a fairly strong January and February 2020.

GC: Which region comes out least affected according to your research?

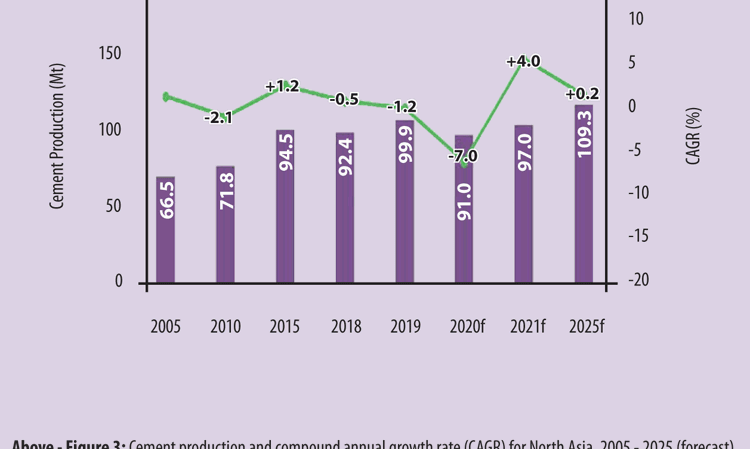

JH: Least affected will be definitely North-East Asia, which comprises Japan, South Korea, Taiwan, Mongolia and North Korea. South Korea contained the coronavirus better than any other country, the active cases peaked in mid-March 2020.

Japan and Taiwan are also on a good track, however due to some early lockdown release Covid-19 cases have increased slightly again. Regarding our projection for cement production, we expect only a decrease of 7.0% in this region.

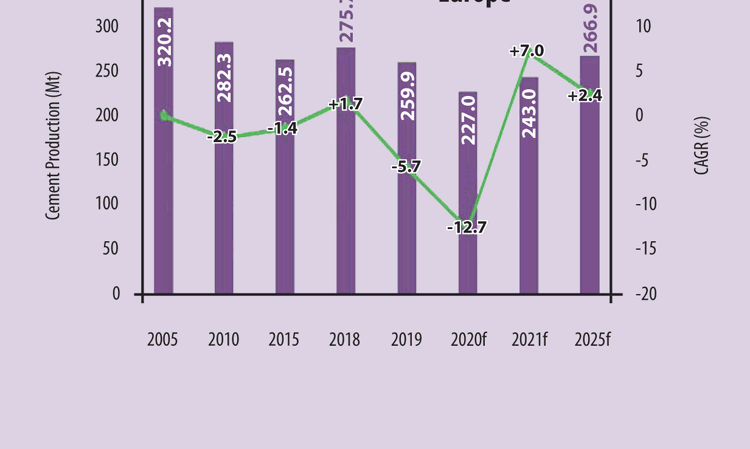

Our projection for Europe as a whole is a 12.7% decrease in cement production. However, we have a breakdown into four sub-regions: Northern, Western, Southern and Central Eastern Europe/Turkey. The Southern region, which includes Italy, Spain, Portugal and Greece, will be mostly affected, with declines in cement consumption of up to 16% in individual countries.

The US still has to decrease its active load of Covid-19 cases, although the construction sites are still open in about 80% of the states. At the moment it is not clear how this situation will change. In our projection we anticipate a decline of 11.2% for the US in 2020 and about 10% for Canada.

GC: What else does the report contain?

JH: We also looked to the capacity utilisation figures, with forecasts for 2020, 2021 and 2025. These show some interesting trends compared to the situation in 2019. In the immediate future, we expect capacity utilisation in 2020 to ‘crash.’ China operated at 74% capacity utilisation in 2019 and we forecast 70% in 2020. The rest of the World will see capacity utilisation slump from 60.8% in 2019 to 53.8% in 2020. This means that there won’t be a large shortage of cement, even if half of the world’s cement plants are forced to close due to the virus! On the contrary, the closure of cement plants by producers is necessary to remain profitable.

Between 2019 and 2025, we expect that China will lose around 570Mt/yr of cement production capacity and cut production by around 500Mt/yr. In the rest of the World, we expect that both production and capacity will rise, by 284Mt/yr and 250Mt/yr respectively.

Notice here, something interesting. The increases in the rest of the World figures will not make up the drop in China. Overall production will fall by 216Mt/yr between 2019 and 2025. Global cement capacity will fall by 320Mt/yr.

GC: Thank you for a very interesting discussion.

JH: Thank you for letting me share this information with your audience.